The resurgence of emerging markets exchange traded funds has received ample and deserving attention this year. Year-to-date performances by the Vanguard FTSE Emerging Markets ETF (NYSEArca: VWO) and the iShares MSCI Emerging Markets ETF (NYSEArca: EEM), the two largest emerging markets ETFs by assets, highlight why investors have returned to emerging markets ETFs.

And returned they have. Since the start of the third quarter, EEM and VWO have hauled in $2.8 billion and $2 billion in new assets, respectively. No ETFs have been in terms of third-quarter inflows. Over that time, VWO and EEM are up an average of 3.6%, but a familiar face is starting to once again make its presence felt among emerging markets ETFs.

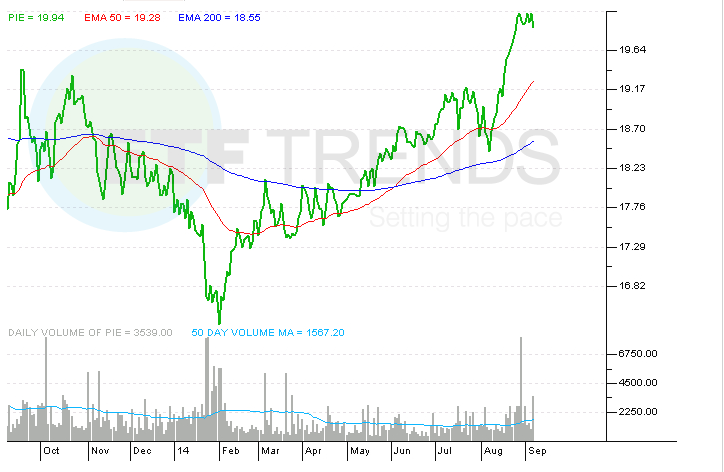

With momentum returning to developing world equities, the PowerShares DWA Emerging Markets Momentum Portfolio (NYSEArca: PIE) is once again flexing its muscles with a third-quarter gain of 4.7%. Investors have responded, having poured $50.5 million in new assets into PIE over the past month, a total surpassed by only three PowerShares ETFs, according to issuer data.

Like some U.S.-focused ETFs that overtly espouse the virtues of momentum in their names, PIE’s status as a momentum ETF can lead some investors to believe the fund is something it is not. Just as some U.S.-focused momentum ETFs are not chock full of biotech, social media and other so-called momentum stocks, PIE is not always littered with the highest beta and most volatile emerging markets. [A Slice of PIE]

At the moment, PIE is actually rather light on emerging markets that fit the bill as “momentum markets” (think Indonesia and the Philippines). India is not even part of PIE right now.

What is crucial to remember with PIE is that the Dorsey Wright Emerging Markets Technical Leaders Index, PIE’s underlying index, is built on price momentum, which can apply to a plethora of countries and stocks. As PIE highlights, there is a big difference between positive price momentum, which is not confined by sector, and momentum as it applies to biotech or Internet stocks. [Some Enhanced ETFs Beat Their Benchmarks]

PIE is currently tilted away from perceived momentum emerging markets and heavily allocated to two of the developing world’s most advanced and lowest beta countries: South Korea and Taiwan. Those countries combine for 39% of the ETF’s weight, indicating a momentum ETF can also credibly sport conservative credentials.

Sometimes forgotten in the discussions of PIE’s merits is the ETF’s sector composition. This is not the run-of-the-mill emerging markets ETF dominated by the energy, financial services and materials sectors or some combination of the three. In fact, those sectors combine for just 19.4% of PIE’s weight.

PIE is more levered to the emerging markets consumer story with a combined 34.3% weight to discretionary and staples stocks as well as being more exposed to the improving exports theme with a 16.1% tech weight.

PowerShares DWA Emerging Markets Momentum Portfolio

{kind=link}

Tom Lydon’s clients own shares of EEM.