The resurgence of the U.S. dollar has been impactful beyond forex pairs and dedicated dollar exchange traded funds.

Due in large part to the dollar’s strength and accommodative monetary policies from the Bank of Japan and the European Central Bank, these are halcyon days for currency hedged ETFs.

Back in the days of acute dollar weakness, investors could look past the erosive impact of currency fluctuations because the tumbling dollar made returns for some global ETFs appear rosy. However, when the weak dollar was stripped from the equation, those returns were not as impressive as previously believed, a fact that has validated the rise of currency hedged ETFs. [Currency Hedged ETFs on the Rise]

The ascent of currency hedged ETFs has been led by Japan-focused funds, such as the WisdomTree Japan Hedged Equity Fund (NYSEArca: DXJ) and the Deutsche X-trackers MSCI Japan Hedged Equity ETF (NYSEArca: DBJP), with European offerings the WisdomTree Europe Hedged Equity Fund (NYSEArca: HEDJ) and the Deutsche X-Trackers MSCI Europe Hedged Equity ETF (NYSEArca: DBEU) soaring to prominence this year. [Hedged Euro ETF Looks Good]

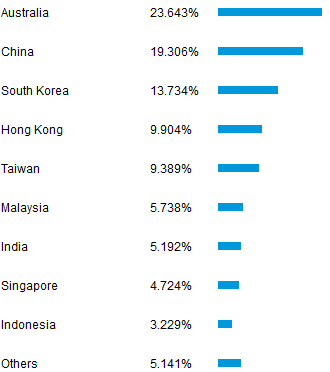

Lost in the shuffle has been the DeutscheX-trackers MSCI Asia Pacific ex Japan Hedged Equity Fund (NYSEArca: DBAP), an ETF deserving of more attention than it has received to this point. DBAP, which is less than two weeks shy of its first anniversary, can be looked at as a currency hedged equivalent of the iShares MSCI Pacific ex Japan ETF (NYSEArca: EPP). However, it must be noted that EPP features notable exposure to just five countries. On the other hand, at least eight countries are somewhat well-represented in DBAP’s portfolio, according to issuer data.

Like DBEU and HEDJ, which are outperforming their unhedged Europe ETF counterparts, DBAP, despite its unheralded status, is up 6.5% this year. That is more than double the gain offered by EPP.

Part of DBAP’s allure comes from its 23.6% weight to Australian equities. Even with the Australian dollar’s status as one of the most traded currencies in the world, ETF issuers have not gotten around to introducing a hedge Aussie dollar product in the U.S. Without such an ETF available, DBAP is one of the best equity-based avenues for profiting from the decline of the Aussie.

And declining is just what the Australian dollar is doing. Over the past three months, the CurrencyShares Australian Dollar Trust (NYSEArca: FXA) is off nearly 6%. Although it appears unlikely the Reserve Bank of Australia will lower interest rates again (Australia’s benchmark rate is a record low 2.5%), RBA has not been shy about saying it continues to view the Aussie as too expensive. [Upside for Australia ETFs]

With South Korean stocks accounting for 13.7% of DBAP’s weight, the ETF has benefited from recent weakness in that country’s won. The South Korean currency currently labors around five-month and to due to its intense export battle with Japan, South Korea’s efforts to weaken the won, though speculative at this point, cannot be deemed out of the realm of possibility, either.

Deutsche X-Trackers MSCI Asia Pacific ex Japan Hedged Equity ETF Country Lineup

{kind=link}

Chart Courtesy: Deutsche Asset & Wealth Management