Despite some high-profile scares in the municipal debt market, muni bonds and related exchange traded funds are still a relatively safe asset class, provide attractive tax-equivalent yields and offer increased diversification.

On a recent webcast, What’s Next for Municipals?, Blair Ridley, Director and Portfolio Manager for Deutsche Asset & Wealth Management, points out that the majority of municipalities are on a strong footing.

“Municipal revenues continue to increase and defaults continue to decline,” Ridley said.

State collections have increased for 16 consecutive quarters after declining five straight quarters during the recession. Municipalities have also kept their debt-to-GDP relatively stable over the past five decades. State and local debt-to-GDP have remain below 20%, whereas federal debt ratios have increased to over 100%.

Moreover, credit agencies have recently upgraded some states’ credit ratings due to their decreasing budget deficits, including California and New York. [California Muni Bond ETFs Look Golden]

The muni market is also being supported by a record low supply of new issuance. Some analysts expect new issuance of $300 billion or less in 2014. [Muni ETFs Supported by Lowest New Issuance Since 2001]

The recent swings in the munis market are attributed to the high-profile bankruptcy filings in Detroit, Michigan and Stockton, California, along with financial problems in Puerto Rico. Specifically, general-obligation bonds, which are backed by credit an the taxing ability of the issuing municipality, are under increased scrutiny as some cities fail to generate enough tax revenue to cover their debt.

Alternatively, investors can consider the db X-Trackers Municipal Infrastructure Revenue Bond Fund (NYSEArca: RVNU), the first ETF to focus exclusively on revenue bonds.

Sean Edkins, Director and ETF RVP for Deutsche Asset & Wealth Management, explains that the ETF tracks bonds that fund federal, state and local infrastructure projects such as water and sewer systems, public power systems, toll roads, bridges, tunnels, and many other public use projects where the interest and principal repayments are generated from dedicated revenue sources.

Municipal bond investors can enjoy attractive yields, especially those who are in higher income brackets. After the tax hikes in 2013, investors in the top bracket generated a 6.18% tax-equivalent yield in 2013, compared to a 5.38% tax-equivalent yield in 2012, on muni bonds with an average 3.5% yield.

Furthermore, muni investors offer attractive diversification benefits, showing a low correlation to equities and other fixed-income assets.

“Municipal bonds have historically provided attractive risk/return characteristics, particularly when tax benefits are considered,” Blair added.

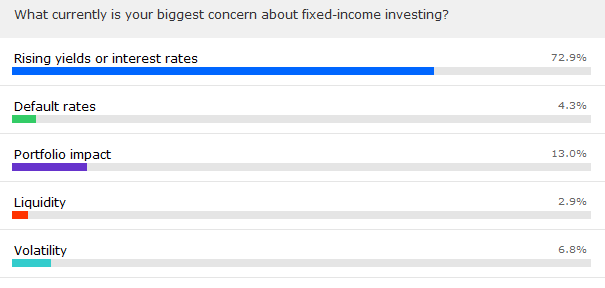

According to a recent survey, many advisors are concerned about rate risk ahead. Christina M. Wagner, President of EagleView Capital, though, argues that investors are better served sticking to intermediate-term debt, or bonds with a five to seven year duration. Rates remain low as demand and short-term keep a lid on yields.

{kind=link}

Financial advisors who are interested in learning more about municipal bonds can listen to the webcast here on demand.