Tape watchers and daily chartists could have a field day on some of the out of the ordinary intraday trading activity we have seen this week in certain ETFs, particularly in the Fixed Income segment, affecting High Yield Corporates (HYLD, JNK) and even some Treasury linked ETFs like UST for example.

It has simply consisted of notable price dislocation and disagreement in the market place at times, potentially sloppy at times as well and in some isolated cases with “head for the exits” aggressive trading in certain fixed income products.

There have been more than a handful of notable short term deviations from the ETF’s trading price versus where one would value the fund’s “NAV” but then again this would not be the first time we have seen such “tells” materialize in the market in times of short term macro/global distress (Russia/Ukraine, Puerto Rico, Argentina, Portugal, etc.).

Dislocations like this also provide managers and institutions whom may be on the sidelines with lower than optimal allocations to fixed income the opportunity to take long positions, so in short, disarray often creates opportunity.

We do recall late last week an analyst call coming out of Goldman Sachs that in a nutshell expressed concern with a fixed income sell-off leading to equity market weakness, which has absolutely materialized this week and in short order. With massive assets in the largest Bond ETFs (BND $21 bln, AGG $18 bln, LQD ($17 bln), BSV ($14 bln), TIP ($13 bln), HYG ($12 bln), CSJ ($11.8 bln), JNK ($9.2 bln) and the list goes on. In fact, the roster is so deep in the broad “Fixed Income” ETP category that a total of forty one ETPs that have greater than $1 billion in assets under management, so anytime the markets receive a jolt of volatility or potential dislocations, you can expect flows to occur as asset managers try to navigate from one segment to another within the bond markets via said ETFs.

Since the realm of Fixed Income ETFs can be quite daunting, with 269 listed ETPs in the U.S. landscape currently targeting areas as different as U.S. Treasuries and Emerging Markets corporate bonds, numerous items need to be taken into consideration outside of simple price/yield analysis when determining where and when allocations should and will occur.

We expect that rotation will continue in this space so long as global/macro tensions of the day remain high and as profits have rapidly disappeared in some segments in FI, some holders that may have initially owned certain bonds for reasons of yield, may look for reasons to take shelter and take some chips off of the table going into the fourth quarter.

On the other hand, those under-allocated to High Yield, or even U.S. Treasuries, may be very eager to establish long positions at these “drawdown” levels, and we have seen noticeable nibbling in both segments and related ETFs not only yesterday but early this morning.

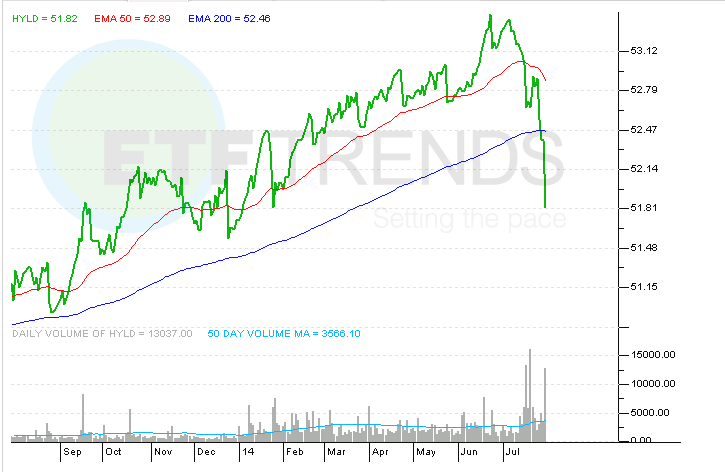

AdvisorShares Peritus High Yield ETF

{kind=link}

For more information on Street One ETF research and ETF trade execution/liquidity services, contact Paul Weisbruch at pweisbruch@streetonefinancial.com.

Street One Financial is an educational/research firm utilizing the Broker Dealer services of Precision Securities, a FINRA registered Broker/Dealer.