The history of preferred stock exchange traded funds in the U.S. is an interesting one.

The iShares U.S. Preferred Stock ETF (NYSEArca: PFF) and the PowerShares Preferred Portfolio (NYSEArca: PGX), by far the two largest preferred ETFs, debuted in early 2007 and 2008, respectively, but what initially looked like dubious timing for any new ETF, particularly in the case of PGX, would prove to be anything.

Thanks to a spate of new preferred issues from large financial institutions needing to appease the Treasury Department coupled with the Federal Reserve’s quantitative easing and zero interest rate policies, preferred ETFs would become a favored asset class for income investors following the financial crisis. [Preferred ETFs Eye New Highs]

The universe of preferred ETFs has since evolved to include funds that include significantly less exposure to the financial services sector and even international preferreds. Don’t scoff at those niche approaches. Some highly focused preferred ETFs have proven successful. [Income ETFs Haul in Assets]

The PowerShares Variable Rate Preferred Portfolio Fund (NYSEArca: VRP), the newest kid on the preferred ETF block, is showing signs of success and impeccable timing. Investors in some of the of the aforementioned preferred ETFs and others undoubtedly remember the struggles of these funds last year when Treasury yields spiked.

Those struggles reminded investors that there is a price to pay with the tempting yields offered by preferred stocks and ETFs. That being a sensitivity to rising interest rates and while Treasury yields have fallen this year, the reality is rates will rise again at some point.

We will not be so ambitious as to say exactly when, but it is not far-fetched to imagine VRP proving durable in a rising rate environment. After all, the ETF is designed to do just that.

VRP could prove attractive to income investors when interest rates rise because most preferred shares are either perpetual or sport long durations, making the issues sensitive to higher rates. Variable-rate preferreds usually carry lower interest rates than fixed-rate preferreds of comparable credit quality. However, the trade-off there is an ETF such as VRP should be less sensitive to interest rate changes. [Falling Rates Lift Preferred ETFs]

The new ETF traded $1 million notional in its first day of trading and has since proven that was no fluke, amassing $17.6 million since its May 1 debut.

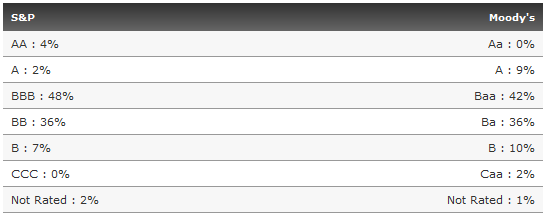

Of VRP’s 86 holdings, 84% are rated BBB or BB by Standard & Poor’s. The new ETF has a 30-day yield of 4.62%. That is about 150 basis points lower than 30-day SEC yield on PGX, but 200 basis points above 10-year Treasuries.

PowerShares Variable Rate Preferred Portfolio Fund Credit Quality

{kind=link}

Table Courtesy: PowerShares