There are myriad ways for investors to gain emerging markets exposure with exchange traded funds with the most common being diversified, multi-country funds that weigh components by market value.

That usually means ample exposure to China, South Korea, Taiwan and Brazil along with a hefty allocation to the financial services sector. In terms of holdings, common placeholders in many diversified emerging markets ETFs include Taiwan Semiconductor, and if the ETF values South Korea as an emerging market, Samsung.

These funds are also, in many cases, exposed to massive state-controlled enterprises, usually hailing from the financial services, energy and materials sector. [Brazil ETFs Almost Attractive]

A new ETF, the EGShares Blue Chip ETF (NYSEArca: BCHP) eschews the common ETF approach to emerging markets exposure. Rather than hold companies based in emerging markets, BCHP leverages developed market firms that derive significant portions of their revenue from the developing world.

“Some of the companies tracked by the big emerging markets ETFs are giant multinationals that get large portions of their revenue from developed markets. This ETF could lead a new wave of ‘economic exposure’ ETFs that aren’t interested in where a company is domiciled but rather in where its revenue comes from,” reports Eric Balchunas for Bloomberg.

While BCHP’s approach may be unique, a deeper look at the new ETF’s construction turns up a familiar methodology along with plenty of familiar constituents.

BCHP, which debuted in late April, is an equal weight ETF with each of 30 components garnering an allocation of 3.33%. Those 30 holdings include plenty of familiar companies based in the U.S. and other developed markets, such as Qualcomm (NasdaqGS: QCOM), Anheuser-Busch InBev (NYSE: BUD), Colgate-Palmolive (NYSE: CL), Las Vegas Sands (NYSE: LVS) and YUM! Brands (NYSE: YUM). [Blue Chips and Emerging Markets]

BCHP’s holdings derive anywhere from 26% to 100% of sales from emerging markets, according to Bloomberg.

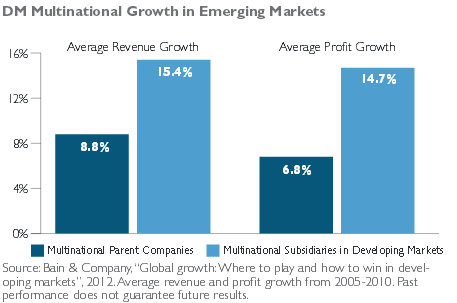

Many investors know the temptation and disappointment of emerging markets, but the data confirm the validity of BCHP’s approach. Average revenue growth in multinational parent companies has been 8.8%, compared to 15.4% for multinational subsidiaries in developing markets while average profit growth has been 6.8% in multinational parent companies, compared to 14.7% in multinational subsidiaries in developing markets, according to EGShares data.

Due its developed market lineup, BCHP sports a valuation that is rich compared to most emerging markets. The ETF’s underlying index, the EGAI Developed Markets Blue Chip EM Access Index, has a trailing P/E of 19.5, according to issuer data. The MSCI Emerging Markets Index trades around 10 times earnings.

{kind=link}