As share buybacks by U.S. companies have increased, so has the allure of exchange traded funds that use buybacks as the cornerstone of their weighting methodology.

S&P 500 members spent $129.4 billion on share buybacks during the fourth quarter of 2013, up from $128.2 billion in third quarter. For all of last year, S&P 500 constituent companies spent $475.6 billion on buybacks, up from $398.9 billion in 2012, according to S&P Dow Jones Indices data. [Buyback ETF Still Shines]

It must be noted that not all buyback or float shrink ETFs are created equal. Take the example of the actively managed TrimTabs Float Shrink ETF (NYSEArca: TTFS). TTFS has $125.5 million in assets under management,$110 million of which has come into the ETF over the past 12 months, indicating interest in the fund is rising along with positive buyback news. [Float Shrink ETF Tops $100M in AUM]

But TTFS does not just focus on buybacks.

“Buybacks are one element to our strategy, but TTFS is not just another buyback ETF,” said TrimTabs Portfolio Manager Minyi Chen in an interview with ETF Trends.

It is one thing for a company to make a buyback announcement, but it is another thing altogether for that company to resist the temptation of increasing its float with executive stock options, which can mitigate the float shrink impact of the announced repurchase program.

For example, Costco (NasdaqGS: COST) authorized a buyback program in the amount of $4 billion in April 2011, expiring April 2015. As of March 2014, the company has spent $1 billion on buybacks, but the total shares outstanding actually increased from 437.8 million to 439.9 million, which suggests that the company issued more shares than they have repurchased.

As Chen points out, how companies repurchase their shares is a pivotal ingredient in the TTFS recipe.

“We care about how companies reduce their net equity float,” he said. “We prefer companies that use free cash flow to repurchase shares rather than issuing debt to do buybacks.”

That is an important factor to consider because the rise in buybacks has coincided with the Federal Reserve’s zero interest rate policy, but when interest rates rise, companies that have borrowed heavily to fund repurchase programs could be crimped by those higher rates. [Opportunity With Buyback ETFs]

“Avoiding companies that borrow to repurchase shares offers TTFS downside protection if rates rise,” said Chen. “In general, companies with higher leverage are riskier and more volatile. Ultimately, the TTFS free cash flow screen is good for investors.”

It is hard to argue with the results. TTFS, which turns three in October, is up 91.25% since coming to market, according to Morningstar data.

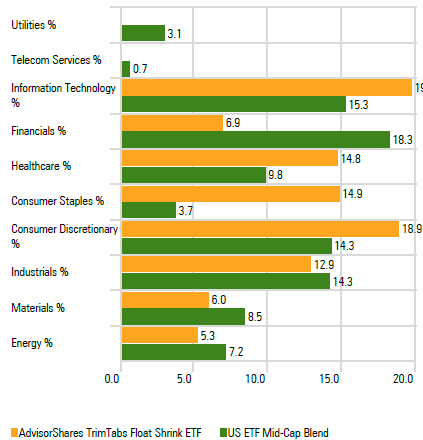

As Chen notes, the ETF’s equal weight strategy has served it well. TTFS holds 100 stocks, none if which account for more than 1.1% of its weight, according to AdvisorShares data. TTFS is also diverse at the sector level with consumer discretionary, industrial, technology, health care, staples and financial services names all receiving double-digit sector weights.

Chen said TTFS was purposefully designed as an equal weight ETF because of the long-term track record that strategy has, noting that TTFS has a lower beta and is less volatile than an equal version of the S&P 500 even though it has more exposure to mid- and small-caps on a percentage basis.

TTFS Sector Weights

{kind=link}

*Data as of March 31, 2014

Chart Courtesy: AdvisorShares

Tom Lydon’s clients own shares of TTFS.