If finance were high fashion, ‘smart beta ETFs’ would be the showcase of this year’s Spring collection. They are receiving a lot of press attention and surveys of institutional investors show that they plan to increase their adoption of smart beta ETFs. In this article, we answer the question: What specifically are smart beta ETFs and what assets have they gathered to date? Looking beyond the label is very important to both retail and institutional investors.

To do this, we first need to define ‘traditional’ beta ETFs. In its purest form, an ETF providing ‘traditional beta’ exposure is one that tracks a market capitalization weighted broad market index. So if this is traditional ‘beta’, then what is a ‘smart beta’ ETF?

A theoretician may define it as an ETF providing index-based exposure to any investment risk factor other than broad market risk. By this narrow yardstick, even an ETF that tracks the S&P Small Cap 600 could be considered ‘smart beta’ since it provides targeted exposure to the ‘size’ risk factor. Taking this definition very literally, even an ETF that tracks the S&P 500 wouldn’t be ‘pure’ beta exposure, since the S&P 500 screens stocks for profitability prior to inclusion.

We are more interested in the practitioner’s definition of ‘smart beta’. Here is a working definition of a smart beta ETF:

An ETF that tracks a rules based index providing exposure to a specific investment risk factor other than market cap weighted size, style (growth/value) or industry sectors.

We can break down this definition into its key components:

Index based: This eliminates ‘active’ ETFs i.e. those that don’t track an index. Essentially ‘smart beta’ ETFs are ‘index-izing’ what may earlier have been marketed as an active strategy. As I argued 2 years ago on Seeking Alpha, this represents a blurring of the distinction between traditional ‘passive’ and ‘active’ investing.

Specific risk factor: These ETFs should give you access to a targeted, definable risk factor or strategy such as low volatility, momentum etc. We exclude quantitative strategy ETFs even if they are index based, if the targeted risk factor or strategy is not tightly defined.

Excluding cap weighted size, style and sectors: This is clearly a judgment call, but a useful and important one. The practice of index based investing in market cap weighted size (e.g. small cap), style (e.g. value) and industry sectors has been well established for several years. Through the term ‘smart beta’ we are trying to identify those strategies that investors did not have access to via low cost, index-based products till recently. We also exclude inverse & leveraged ETFs.

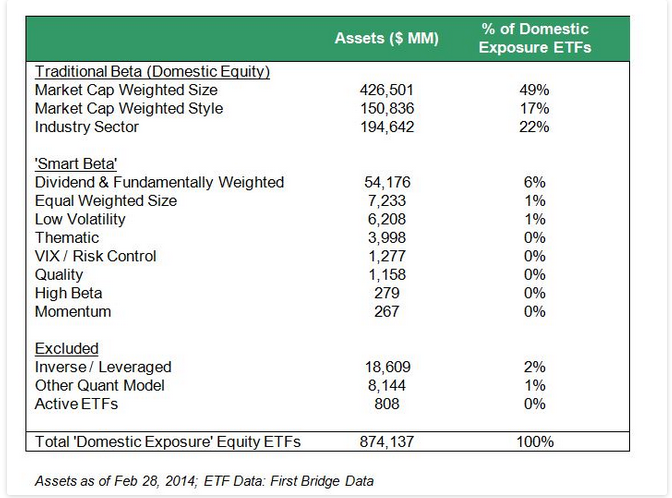

The table below shows the assets for US listed ETFs that provide domestic US equity exposure. It shows the breakdown of assets into ‘traditional beta’, ‘smart beta’ and ‘other’ categories based on our definition above. The ETF Data (ETF classifications and assets) is from the First Bridge ETF database.

{kind=link}

As we can see, ‘smart beta’ currently accounts for a sizable $75B in assets (or almost 9% of assets for US listed ETFs that provide domestic equity exposure). Given the interest in this space, we can expect this percentage to grow. At some point this has to hit a natural limit, since by definition, market participants in aggregate need to hold the market portfolio. However since ETFs as a category are still a minority of assets relative to mutual funds and individual security holdings, theoretically there is still adequate headroom for growth.

While ‘smart beta’ is a snappy marketing phrase, it could misleadingly imply that investing in these ETFs is ‘smarter’ than investing in traditional market cap weighted broad market ETFs. In reality, different risk factors will perform differently across market cycles. For example:

- Volatility vs. High Beta: The S&P High Beta Index has performed extremely well in the trailing 5 years (28% annualized total return through 3/17/14) vs. 19.5% for the S&P Low Volatility Index. This is to be expected since we are 5 years from the trough in March 2009, and the S&P 500 has had an annualized total return of 21.6% since that time. Going forward however, the current crisis in Ukraine, the slowdown in China and the relatively high equity valuations in the US could weigh on the market, and a rotation back into Low Volatility is likely.

- Equal Weighted vs. Market Cap Weighted: In the same trailing 5 years, the S&P equal weight index has significantly outperformed the S&P 500 (27% annualized TR vs. 21.6%). This is because equal weight ETFs are essentially providing a tilt towards relatively lower cap stocks, and mid-cap and small cap stocks have significantly outperformed large caps in this period. Once we move into a market environment where investors are more risk averse, we can expect this performance differential to reduce. In the case of equal weighting however (unlike with low volatility), its advocates will argue that its superior performance may persist relative to traditional cap weighting due to the ‘size premium’.

In conclusion, we estimate the size of the smart beta ETF space for domestic US equity exposure is already about $75B or 9% of the total ETF assets for domestic US equity. However ‘smart beta’ does not imply that these products will always outperform traditional market cap weighted products. Once we move into a more volatile environment, investors will rotate from high beta into low volatility ETFs and the performance differential between equal and cap weighted ETFs will reduce.

This article was written by Aniket Ullal, founder of First Bridge Data.

© S&P Dow Jones Indices LLC 2013. Indexology® is a trademark of S&P Dow Jones Indices LLC (SPDJI). S&P® is a trademark of Standard & Poor’s Financial Services LLC and Dow Jones® is a trademark of Dow Jones Trademark Holdings LLC, and those marks have been licensed to SPDJI. This material is reproduced with the prior written consent of SPDJI. For more information on SPDJI, visit http://www.spdji.com.