They have been the brightest spots among sector and sub-industry exchange traded funds this year, but a valuation anomaly could be cause for concern regarding health care ETFs.

For the first time since 2006, the health care sector is pricier, albeit slightly, than consumer staples. In terms of big-name ETFs, the Health Care Select Sector SPDR (NYSEArca: XLV) sports a P/E ratio of 17.54 compared to 17.5 for the Consumer Staples Select Sector SPDR (NYSEArca: XLP), according to State Street data.

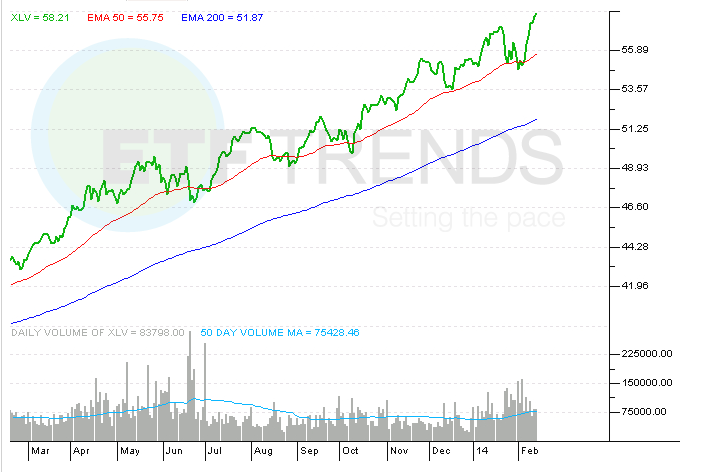

The gap is small, but it does come at a time when XLV is printing new all-time highs and XLP is down 1.4% year-to-date. When accounting for dividends paid, XLV topped XLP by more than 1,500 basis points last year. [Staples ETFs Struggling in 2014]

The cautionary tale is that in 2006, XLP outpaced XLV by 810 basis points, the same margin by which the health care ETF lagged the S&P 500. Biotechnology stocks, which account for nearly 20% of XLV’s weight, explain a good part of XLV’s slight premium to XLP. [Health Care ETFs Show Strength]

Bank of America Merrill Lynch’s Savita Subramanian “points out that Healthcare is now trading at a premium to Consumer Staples for the first time since 2006. Biotechnology stocks within the Healthcare sector have had a lot to do with that. The report says that Biotech is now selling at a 60% premium to the S&P 500 on a forward PE basis – which is double the premium it has historically traded at,” according to Josh Brown on The Reformed Broker.

In 2006, the iShares Nasdaq Biotechnology ETF (NasdaqGS: IBB) and the SPDR S&P Biotech ETF (NYSEArca: XBI), which debuted in late January of that year, both finished in the red.

A couple of things are notable about health care’s premium to staples. First, as the chart here shows, the scenario, although not seen since 2006, is not all that rare. For example, from 1986 to 2003, health care was frequently more expensive than staples. Second, over the six years ending 2013, XLV and XLP’s head-to-head competition is a draw at three annual wins for each ETF.

What has some concerned about further upside for health care stocks and ETFs is the aforementioned frothy valuations for the biotech sub-sector. Some may even be focusing on the fact that IBB has been one of the 10 best non-leveraged ETFs of any type for three consecutive years, reasoning that the largest biotech fund needs to run out of steam at some point. [One Biotech ETF Standout]

There is no denying that biotech stocks are expensive, but consider this: The combined P/E ratios of Biogen (NasdaqGM: BIIB), Amgen (NasdaqGM: AMGN), Gilead (NasdaqGM: GILD), Celgene (Nasdaq: CELG) and Regeneron (NasdaqGM: REGN) – roughly 37% of the Nasdaq Biotechnology Index’s weight – is nearly 239.

Said another way, the combined P/E of those stocks is barely above that of Netflix (NasdaqGM: NFLX) and not even half that of Amazon (NasdaqGM: AMZN). Amazon trades at over 84 times forward earnings, or nearly double Regeneron’s forward P/E.

No, the comparison of biotech to consumer discretionary stocks is not apples-to-apples. And yes, biotech is expensive, but maybe, just maybe the premium is justified. Perhaps it is trite to say, but Amazon and Netflix are developed world indulgences while the holdings in biotech ETFs are attempting to make products that improve and save lives.

That might be an inconvenient truth to some, but it could also explain why Amazon’s 95.8% two-year gain looks paltry compared to the 116.3% gained by IBB over the same period. That is not some crazy, one-off example, either. Over the past three years, XLV is up almost 91% while the NASDAQ 100 is up about 59%. [Health Care Delivering as Other Sectors Lag]

Health Care Select Sector SPDR Fund

{kind=link}