CEILINGS, SHUTDOWNS & TAPER

When it’s all said and done, the government shutdown will likely have only a minor impact on fourth quarter GDP. The greater question is what impact this will have on confidence across corporations, consumers and investors. Recent data suggests that economic confidence was negatively impacted by Washington’s lack of resolve. Markets, however, seemed to have shrugged off the turmoil relatively easily, but that may not have been the case if monetary policy conditions weren’t as accommodative.

So, President Obama’s decision to nominate Janet Yellen to succeed Ben Bernanke as the Chairman of the Federal Reserve amid the over two-week government shutdown warrants further attention. Most portray Yellen as an ultra-dovish economist, and while she’s certainly in the accommodation camp, that characterization is an oversimplification.In fact, one of reasons for this recent portrayal has been based on her less than rosy outlook for US economic growth and the lack of a pickup in inflation. Unfortunately she’s been accurate as the economy continues to exhibit significant slack even at this stage of the recovery.

So, what can we expect from her atop the Fed? Based off of her record, she’ll likely be a Fed Chair with an intense reliance on economic models, especially in regards to the path for employment. Today’s low levels of inflation and continued deflationary forces provide cover for further accommodation. The FOMC certainly remains concerned with the tightening of financial conditions, especially since mortgageapplications fell when rates increased. Yellen will continue with Chairman Bernanke’s focus on greater transparency and more open communication.

In fact, Yellen will likely further strengthen this approach in regards to forward guidance. She’ll also be more willing to make her specific views heard than Bernanke did. This may help avoid the miscommunication around this summer’s taper trade. We will need to see firmer employment data before the Fed is comfortable dialing back even as some become increasingly concerned with the broader impacts to speculative activity.

{kind=link}

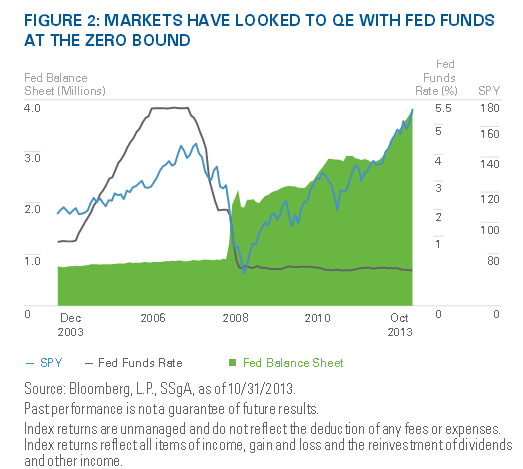

With Bernanke ending his term at the end of January, Yellen will be tasked with implementing and executing the Fed’s exit strategy from its great monetary policy experiment. The Fed’s balance sheet expansion under QE has been a powerful force in propelling equity markets to all-time highs, as illustrated in Figure 2. While tapering is not tightening in the traditional sense, market participants may want to brace for a period of consolidation now that markets have experienced a sizable re-rating with lackluster earnings growth thus far in 2013.

The S&P 500 Index has not traded below its 200-day moving average all year. Going forward, most believe that markets need to see greater signs of positive earnings growth for further gains. In a worrisome sign, earnings revisions are not terrible, but less than inspiring. In light of this, some investors are tempted to believe that we will likely see the end of the positive market run.

{kind=link}

However, we may simply be entering a new regime where investors are willing to assign a higher multiple to US equities due to the continued low inflation and other asset classes offering less attractive investment opportunities. With this tension between the short-term and long-term playing out, this means that investors may look outside of the US to see further gains, especially since the US has outperformed other countries and regions by wide margins.

While US earnings have recovered to pre-crisis levels, Europe has yet to do so. Stabilizing economic growth coupled with economic reforms and improved credit conditions may be the boost that European shares have needed. In addition, investors will do well to focus on using this as a chance to take on more targeted EM exposures. In 2013, EM economies grew four times faster than developed markets, but this gap will decrease to two times next year. Much of the outlook for emerging markets centers around China, which consensus expects to grow by 7.4% next year averting fears around a hard landing.

As China rebalances its economy to be less export driven, opportunities are arising to add targeted exposures to smaller companies with greater exposure to the growing middle class. Traditional fixed-income investors have seen some reprieve, but the Barclays U.S. Aggregate Index remains in the red year-to-date.

Thus, recent market moves are likely reflective of what the next couple of months may bring until the market begins to price in tapering again. With the long-term picture not changing much, investors may continue to migrate from traditional fixed-income exposures and focus on creating portfolios for today’s and tomorrow’s bondmarkets. Specifically, corporations remain attractively valued from a fundamental and technical perspective. Focusing on floating rate notes, short-term high yield bonds and senior secured loans may offer attractive current income with low interest- rate risk.

CONCLUSION

While Democrats and Republicans will most likely remain out of the limelight for the next couple of weeks, they will have ample opportunity to get back in the spotlight as we close out the year and look to January 15 for answers on government funding and February 7 for resolution on the debt ceiling.

Consensus expectations are that tapering is now an early 2014 event with new purchases under QE3 ending later in the year. With Yellen at the helm, any movement will likely be measured as easy money policies will remain.

What’s interesting is that shorter-term trades to take advantage of oversold and undervalued areas exist. However, investors should not lose sight of the fact that markets will eventually come around to the fact that tapering’s back on the table. In fact, investors with longer horizons may wish to take advantage of the chance to shorten duration in fixed-income portfolios and move away from the most rate-sensitive sectors in the equity market.