U.S. stocks keep racing to record highs. Money is pouring into exchange traded funds, particularly the equity-based variety and to the untrained eye, all would appear to be well as year-end nears.

That is far from the case for select U.S. towns and cities. Awash in unfunded pension liabilities and struggling to generate revenue to pay their public employees, municipalities across the U.S. are in increasingly precarious financial positions.

While Detroit’s bankruptcy, the largest municipal bankruptcy in U.S. history, was not seen as a catastrophe for the muni bond market and the ETFs that hold those bonds, there is no denying municipalities are struggling and bankruptcies are on the rise. [Getting Back to Fundamentals in Muni Bonds]

That does not mean all muni bond ETFs are to be ignored, but the scenario does underscore the utility of the db X-Trackers Municipal Infrastructure Revenue Bond Fund (NYSEArca: RVNU).

Consider the following news flow just this week, courtesy of Mike “Mish” Shedlock of Mish’s Global Economic Trend Analysis. On Tuesday, Moody’s Investors Service, warned Scranton, Pennsylvania “could be facing the threat of default or bankruptcy thanks to a $20 million budget gap for the fiscal year that begins Jan. 1. Scranton has more than $195 million in outstanding debt, according to Moody’s.”

Scranton has $100 million in unfunded pension liabilities. On Wednesday, Shedlock pointed out the “Chicago Park District has more than $1.4 billion in official debt. This includes $40 million in debt related to retiree health care, $426 million in pension debt and $944 million in other long-term debt.

Also on Wednesday, Shedlock highlighted the case of Desert Hot Springs, California, which went bankrupt in 2001. Last week, the city’s interim finance director said another bankruptcy is a real option, noting 70% of the city’s budget goes to police costs, the bulk of which are salaries and pension payments to the California Public Employees’ Retirement System, or Calpers.

Back to RVNU, one of the newer entrants in the muni bond ETF arena. RVNU is the first ETF to focus exclusively on revenue bonds, or those munis that are supported by revenue from projects such as toll roads or bridges. Revenue bonds skirt pension risk, meaning RVNU offers investors the income and conservative posture they’re accustomed to with muni ETFs without the fears of capital loss at the hands of increase muni bankruptcies. [Advisors Like The New Spin on Muni ETFs]

RVNU is up almost 3% in the past month and has gathered $15.1 million in assets since its June debut.

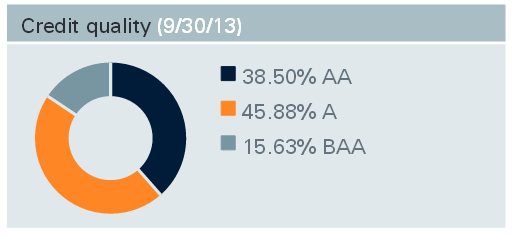

RVNU Credit Profile

{kind=link}