Still, conservative investors may opt to mix to combine PDP and SPLV. That turns out to be a potent strategy as well when a portfolio is 30% allocated to SPLV and 70% allocated to PDP during the best six-month period. The 1997-2011 returns for that strategy were over 336%, according to Dorsey Wright.

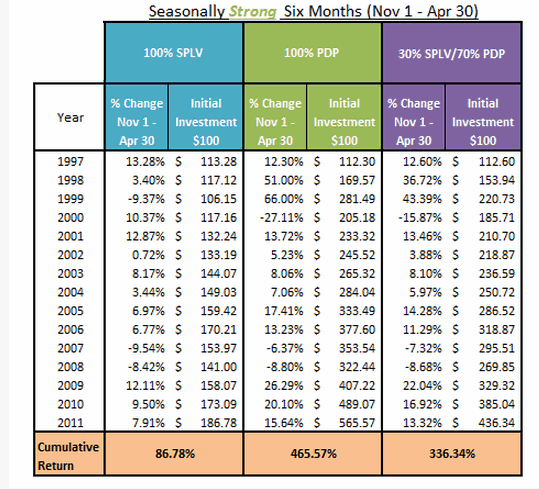

“SPLV has generally provided greater returns during the seasonally weak six months (cumulative of 19.03% since 4/30/1997) than the PDP (-9.48%). However, the SPLV has notably lagged the return, up 86.78%, during the seasonally strong six months of the PDP, up 465.57%. Therefore, a 30% PDP/70% SPLV spit during the seasonally weak six months has seen a cumulative return of 13,37% while a 70% PDP/30% SPLV split during the seasonally strong six months has seen a return of 336.34%,” said Dorsey Wright.

As for the most recent efficacy of the buy PDP and SPLV during the best six months strategy, from November 1, 2012 through April 30, 2013, PDP surged almost 15% while SPLV jumped 16.3%. The S&P 500 was up 13% over the same time.

PDP/SPLV Switching Strategy (click to enlarge)

{kind=link}

Chart Courtesy: Dorsey Wright & Associates