The WisdomTree Emerging Markets Consumer Growth Index (WTEMCG) strives to provide exposure to one of the major macroeconomic themes that we believe will be driving the global economy over the coming years, with a broadly diversified and inclusive approach to selection.

One of the more important questions about WTEMCG is how its sector composition compares to market cap-weighted indexes that many are familiar with and track. Our goal in creating WTEMCG was to provide a differentiated approach to benchmarking a truly unique exposure centered upon a specific theme—which is more than a one-sector idea and encapsulates the broad trends happening in the local economies.

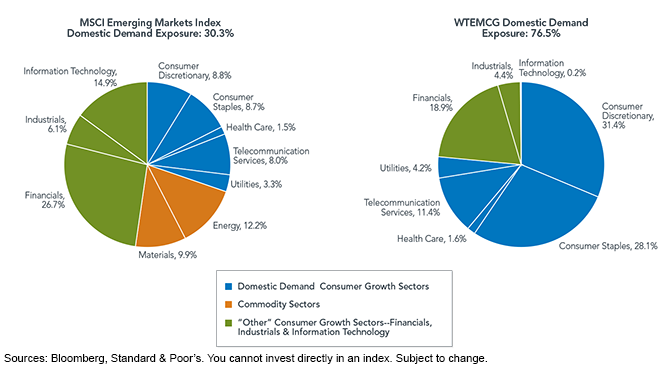

Exposure to Broad Sector Groups

To simplify the analysis, it is helpful to group the 10 sectors into sub-categories that we believe share some common attributes. This, in turn, will allow us to better illustrate the sector exposures of WTEMCG compared to those of other, more broadly focused emerging market equity indexes.

• Domestic Demand Consumer Growth Sectors: These would include Consumer Staples, Consumer Discretionary, Telecommunication Services, Utilities and Health Care. We believe that each of these sectors has a relatively clear-cut rationale for exposure to a growing emerging market consumer base, meaning that as incomes increase, demand for the goods and services produced by firms within these sectors would also be expected to increase.

• Commodity Sectors: Typically, the inputs and outputs of firms within each of these sectors are very heavily exposed to commodities, which we believe makes them much more globally sensitive in that commodity prices are often driven by global events.

• Other Consumer-Oriented Sectors—Financials, Industrials and Information Technology: These three sectors can either be globally influenced or driven more by local EM demand. Certain industrial or technology firms are big exporters and globally sensitive, while others can be more domestically sensitive. The same can be said for in that smaller banks may be in a position to directly benefit from rising incomes across emerging market populations, but larger banks may be more exposed to global risks and less reflective of the theme WTEMCG is trying to capture.

• WTEMCG therefore includes the domestic demand and the local economy and consumer-oriented aspects of other sectors but excludes the commodity sectors. Other commonly used indexes typically include all sectors or narrow their choice down to one or two specific sectors.

Geographic Revenue Rules—The Test Every Constituent Must Pass

A differentiated driver of WTEMCG lies in its geographic revenue rules. Investors often try to get access to this factor in one of two ways:

• Consumer Sectors: Focus on companies within the Consumer Discretionary and Consumer Staples sectors, as the word “Consumer” appears in their names.

• Small Caps: Focus on small-cap companies as opposed to large-cap companies, as large caps, generally speaking, tend to export more than small caps.

However, not all Consumer Discretionary and Consumer Staples companies in emerging markets are purely domestically based, and not all small caps are more locally sensitive.

WTEMCG’s geographic revenue filter identifies constituents that actually generate their revenues predominantly within the emerging markets. The specific revenue screens employed for WTEMCG require:

1. At least 60% of revenue coming from emerging markets

2. Less than 25% of revenue coming from either the United States, Japan or Europe

Domestic Demand Consumer Growth Sector Exposures, as of 8/31/2013

{kind=link}

For definitions of terms in the charts, please visit our Glossary.

• Domestic Demand Consumer Growth Sectors: WTEMCG has over three-quarters of its exposure to this particular sector grouping, compared to the broader MSCI Emerging Markets Index, which has a mere 30% exposure. This shows a dramatic difference in the type of exposure between traditional indexes and WTEMCG, despite the broadly inclusive nature of WTEMCG, with stocks from eight of the 10 sectors.

• Commodity Sectors: We mentioned how these sectors (Energy and Materials) tend to be more globally sensitive. And while WTEMCG excludes them completely, the MSCI Emerging Markets Index has over 20% exposure to them. Many investors think of the emerging markets as being commodity driven, so one way to view WTEMCG is as broad-based exposure to emerging markets that takes away the exposure to the more commodity-sensitive sectors.

• Other Consumer Growth Sectors—Financials, Industrials and Information Technology: The most important element to remember about the firms within these particular sectors that qualify for WTEMCG is that they must pass the aforementioned geographic revenue screens. The MSCI Emerging Markets Index’s exposure to these sectors is approaching 50%, but these firms have not been subject to any geographic revenue screens and consist predominantly of large banks and global exporters—neither of which would be eligible for WTEMCG.

Conclusion

In creating WTEMCG, our overarching goal was fairly simple: to create an Index that provided a diversified exposure to the theme of consumer growth in emerging markets. To truly be successful in its execution, both our sector eligibility and further geographic revenue screens allowed us to more precisely hone in on the types of firms that we wanted to include—and veer away from those that we didn’t. Our sector mix was heavily tilted toward sectors that we classified as domestic demand consumer growth sectors—those that most logically would be associated with increased demand as per capita incomes in emerging markets increased. In the end, we don’t rely on any broad-based generalizations to say that WTEMCG’s constituents generate their revenues from within emerging markets, but on specific screens requiring them to do so.

Jeremy Schwartz is director of research at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.