Gold and silver prices rallied strongly last week after the US passed a bill to reopen the government and suspend the federal debt limit until 7 February 2014.

The rally in gold and silver prices may seem counter-intuitive at first given their safe haven reputations. However, it has to be remembered that both gold and silver prices often have strong negative correlations to movements in the US dollar. Therefore in the run up to the debt ceiling deadline, as US short term rates increased on fears of possible default and the US dollar strengthened, gold and silver prices declined. In a similar manner, when an agreement to raise the debt ceiling was finally signed, US short-term rates and the US dollar fell, and gold and silver prices rallied. Given the rise in COMEX gold futures open interest last week and known large outstanding COMEX gold short positions, the rallies were likely further supported by short covering in the futures market following the agreement. Barring any extreme macro events, we expect the US dollar and rate expectations to continue to drive short term moves in gold and silver prices. With tapering off the table for now, prices may find further short term support.

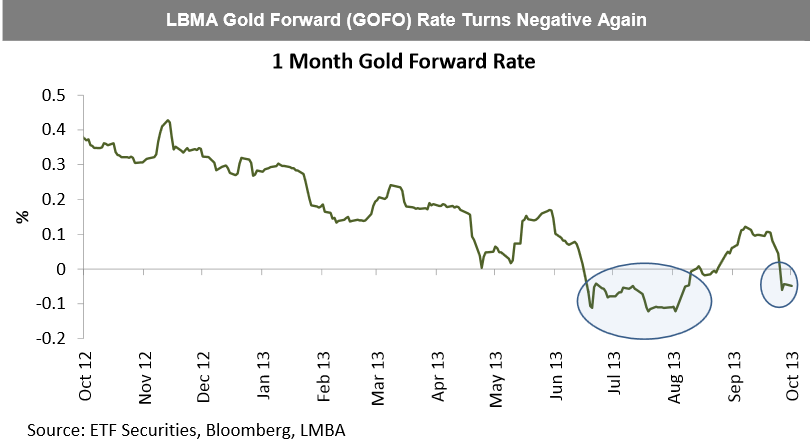

LBMA gold forward (GOFO) rates turn negative again, highlighting physical gold shortage. It is interesting to note that LBMA gold forward rates have again dipped into negative territory, highlighting that physical demand – possibly from central banks as well as short covering – remains strong. This tightness has continued into the new week, indicating this was not solely short term pre-debt deadline hedging and post agreement short covering demand. It seems clear the fact the US debt issue has not been resolved, but only postponed, is accelerating central banks’ and private investors’ search for alternatives to the US dollar as a reserve asset, with gold one of the few viable alternatives.

Platinum and palladium rally on better European auto sales, strong China growth data. The more industrially sensitive precious metals have also started to perform as vehicle sales in China and Europe have improved and China growth has accelerated. European new car sales rose in September, posting the biggest gain in more than two years. European autocatalyst demand remains a keyarea of demand for platinum, second only to Chinese jewellery demand. Additionally, Amplats, the world’s largest platinum producer cited cash operating costs of US$1,740/oz. – approximately 21% above the current spot price. In China, Q3 GDP rose at a higher than expected 7.8%. Continued strength of China’s economy should be positive for both palladium and platinum prices, with palladium benefiting from strong auto sales and platinum from the jewellery sector .

Key events to watch this week. After a dearth of official data, the US non-farm payrolls numbers that will be released tomorrow will likely attract even more attention than usual. Markit PMI manufacturing readings for China and the US will be closely watched as investors assess the impact of the US budget and debt negotiations on global business sentiment.

{kind=link}