We recently had the opportunity to speak with a representative of a fund that launched in February of this year and is unique to the ETF landscape in terms of its makeup and investment strategy. HVPW (ALPS U.S. Equity High Volatility Put Write Index, Expense Ratio 0.95%) is classified as “Long/Short” by databases but this does not necessarily tell the whole story, and it tracks the NYSE Arca U.S. Equity High Volatility Put Write Index.

For those whom might not be intimately familiar with options and much less writing puts, a layman’s explanation of this index is as follows: The index contains large capitalization U.S. listed stocks (20 are held at a time and they roll over every 2 months) that have options listed on them, and selects those put options that have the highest volatility over time.

These options are identified and sold, generating premium income for the ETF investor. In a nutshell, “out of the money” puts are sold on select names within the index, which is a bet essentially that the stocks will not fall below the strike prices on the options themselves.

The specific terms of the put options that are sought out are that they are 60 day listed puts, and the assumption is made that the investor understands as according to fund literature, “Investors assume the risk that the underlying referenced equities may close below their strike price, and investors also give up the upside on the underlying equities above the income the fund receives from selling the options. The strike price of each put option included in the Index must be as close as possible to 85% of the closing price of the option’s underlying stock price as of the beginning of each 60- day period.”

In terms of risks that one accepts in investing in this fund, the investor should understand that the fund “can potentially lose up to the entire strike price of each option it sells” and this would occur of course if put options that are sold close in the money upon expiration. The fund itself attempts to counter-balance this effect with the collection of premium from the puts that it is selling within the portfolio.

To get a flavor of some of the names that are incorporated in the index at the moment (think volatile large cap stocks, and thusthey have linked options that are also volatile), most will not be surprised at some of the following equities: EXPE, RAX, INCY, LNKD, NFLX, FB, GMCR to name just a few.

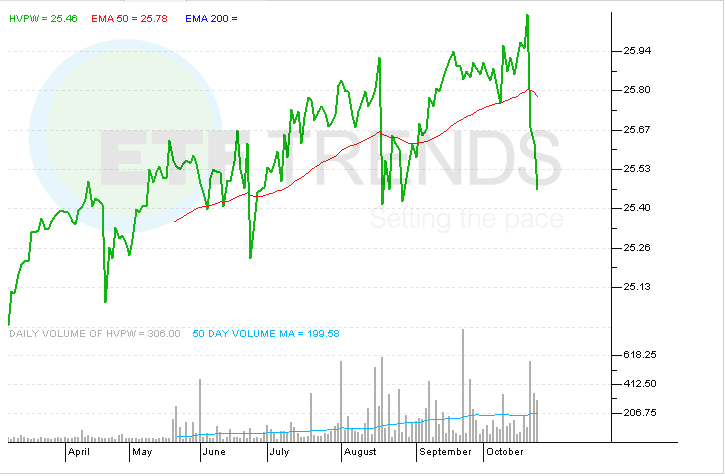

While HVPW has limited live performance and many managers may sit on the sidelines for a bit before leaping into the fund, there appears to be healthy retail and perhaps institutional interest as the trading volume in the fund has steadily climbed over the past several months as the fund has marched higher in terms of price appreciation since inception.

We suspect that portfolio managers that like the idea of incorporating options strategies into their overall plans for ETFs will find appeal in such a strategy, as will those managerslooking for something that generates current income in the form of the distributions that the fund regularly makes (at the end of each 60 day period).

{kind=link}