We conclude our four-post blog series of emerging market equity valuations with a focus on what has become a major theme for equity indexes, emerging market or otherwise: Low volatility. These “volatility-focused” indexes utilize different means for selecting and weighting constituent stocks with a goal of exhibiting lower volatility than do broad market benchmark indexes in different regions.

The Downside to Low Volatility: Potential Lack of Participation in Upside Moves

We believe that when people see the words “minimum volatility” or “low volatility” as part of an index name, they are reminded of their experience during the 2008–09 financial crisis and equate these terms with potential downside protection. Of course, downside protection is one potential effect of a volatility-focused approach, but another effect would be the potentially limited upside capture during a market rally.

Not to mention the thing that a volatility focus ignores completely: fundamentals. That’s not to say that one should focus 100% on potential volatility or 100% on fundamentals—the approaches are totally different, and at times this difference can provide a strong diversification benefit.

We often get asked how the WisdomTree Emerging Markets Equity Income Index (WTEMHY) compares to low-volatility indexes, given its beta of 0.8 since inception. Much of this low beta was a result of its performance in 2008 and 2011. But while the WTEMHY has displayed a low beta since its inception, it is not directly focused on volatility reduction. The methodology of the Index is primarily concerned with identifying the best valuation opportunities in the market, and those sectors can change across time. Currently, the best valuation opportunities can be found in the more cyclical sectors, while some of the lowest-volatility sectors have the richest valuations.

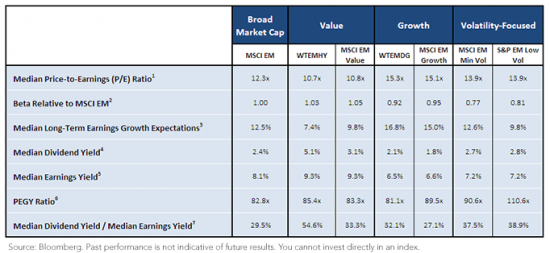

Below, we compare a variety of volatility – and dividend-focused indexes on both a valuation and volatility basis.

As we structure our analysis, we will first outline the indexes that we will be studying.

• MSCI Emerging Markets Index (MSCI EM)

• WisdomTree Emerging Markets Equity Income Index (WTEMHY)

• MSCI Emerging Markets Value Index (MSCI EM Value)

• WisdomTree Emerging Markets Dividend Growth Index (WTEMDG)

• MSCI Emerging Markets Growth Index (MSCI EM Growth)

• MSCI Emerging Markets Minimum Volatility Index (MSCI EM Min Vol)

• S&P BMI Emerging Markets Low Volatility Index (S&P EM Low Vol)

In essence, we will group WTEMHY and MSCI EM Value for their focus on value, albeit in different ways, and similarly we will group WTEMDG and MSCI EM Growth for their focus on growth.

Valuation Ratios for the Value and Growth Oriented Indexes

1Median price-to-earnings (P/E) ratio: P/E ratio of index constituents where 50% of constituent values fall above and 50% fall below.

2Beta relative to MSCI EM: Of the specified index, based on its 7/31/2013 constituents, relative to the MSCI Emerging Markets Index.

3Median long-term earnings growth expectations: Compilation of analyst estimates of the growth in operating earnings expected to occur over the company’s next full business cycle, typically three to five years. Value reflects the point where 50% of values are above and 50% are below.

4Median dividend yield: Value of the trailing 12-month dividend yield for a given index for which 50% of values are above and 50% are below.

5Median earnings yield: Earnings per share divided by share price. Value reflects the point where 50% of values are above and 50% are below.

6PEGY Ratio: Ratio of the median price-to-earnings (P/E) ratio divided by the sum of the median long-term earnings growth expectations and the median dividend yield. Lower numbers indicate lower prices relative to the median long-term earnings growth expectations and median dividend yield of the underlying stocks.

7Median dividend yield/median earnings yield: Meant to calculate the median payout ratio, which is the median dividend per share divided by the median earnings per share.

{kind=link}

Next page: Interpreting the Data

• Beta Analysis: If terms of beta, it is true that MSCI EM Min Vol and S&P EM Low Vol do in fact have the lowest betas of the indexes shown. This is their stated goal—to have relatively lower volatility while still providing exposure to the performance of emerging market equities.

• Volatility Focus Yields Above-Market Price-to-Earnings (P/E) Ratios: The median P/E ratio of MSCI EM is 12.3x, while the volatility-focused indexes all have a median P/E ratio of 13.9x. This essentially gives us an idea: If one were to marry a value index with a volatility-focused index, there could be the potential for a lower beta than that of the value focus as well as a lower median P/E ratio than that of the volatility focus. An added bonus could also be a higher potential dividend yield than for the volatility focus.

• Volatility Focus Yields Relatively High PEGY Ratios: This ratio is a tool with which one can relate the current P/E ratio to the sum of the long-term earnings growth expectations as well as the current dividend yield. WTEMDG, with its high median long-term earnings growth expectations and moderate median dividend yield, looks least expensive by this metric. Both MSCI EM Min Vol and S&P EM Low Vol have relatively higher PEGY ratios because their focus on potentially lowering volatility has led them to stocks with higher median P/E ratios but which don’t necessarily make up for this with high median long-term growth expectations or high median dividend yields.

• Volatility Focus Yields Below-Market Long-Term Earnings Growth Expectations: The long-term earnings growth expectations for the MSCI EM are 13.3%, which is above both the MSCI EM Min Vol and the S&P EM Low Vol indexes. Similar to what we mentioned above, another blend idea could be to combine a growth focus with a volatility focus, if in fact higher potential earnings growth expectations are desired than those accessible with a volatility focus alone.

Conclusion: Complementarity of Fundamentals and Volatility-Focused Approaches

Volatility-focused indexes are great additional tools to consider when thinking about emerging market equities, but no index or methodology can do all things simultaneously. While market capitalization-weighted indexes may be the proverbial blunt instruments, the genesis of new index methodologies allows for indexes to progress further down the path of being precision tools through which to monitor different economic approaches.