Since May, indexes focused on higher-yielding stocks have underperformed the broad market, largely as a result of the steady increase in interest rates.

In a previous blog post, I looked at the overall performance impact the rising interest rates had on different dividend indexes.

Below, I will take a closer look at the performance attribution and underlying exposures that caused the performance divergences.

Federal Reserve (Fed) Taper Talk Caused Interest Rates to Rise

Starting in May this year, longer-term interest rates in the U.S. rose considerably on just a hint the Fed could begin tapering its bond purchases later in the year. Between May 1 and August 20, 2013, the 10-Year Treasury yield increased 118 basis points to 2.81%.1

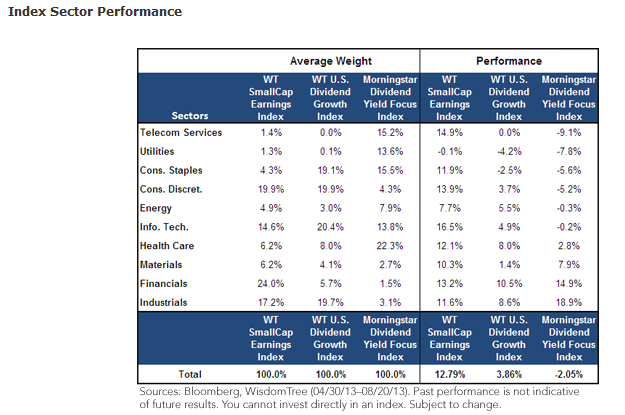

A Detailed Look at Attribution

In the chart below, I take a detailed look at the sector composition and underlying performance of a few indexes that I recently highlighted here. The indexes below include the best-performing of the analyzed indexes (WT SmallCap Earnings), the one with the lowest return (Morningstar Dividend Yield Focus) and one from the middle ground (WT U.S. Dividend Growth) focused on dividend growth that held up better than the high-dividend-yield indexes.

• High-Yield Stocks Underperformed – A look at the Morningstar Dividend Yield Focus Index reveals that the typically higher-yielding sectors (Consumer Staples, Utilities and Telecommunications) had the worst performance since April 30. Each of these sectors represented at least 13% of the index and 44.3% in aggregate.

• Performance Divergences Even among Sectors – Looking at specific sectors across the indexes, we see vastly different constituent performance, which is largely a result of selection methodology. A closer look at the Consumer Discretionary sector reveals how the WT SmallCap Earnings and WT U.S. Dividend Growth Indexes outperformed the Morningstar Dividend Yield Focus Index by 19.1% and 8.9%, respectively, from a stock selection basis. It is also important to note that all the underlying constituents in both the WT U.S. Dividend Growth and Morningstar Dividend Yield Focus indexes are dividend payers, but the WisdomTree Index focuses on potential dividend growers while the Morningstar index focuses on high-dividend yielders.

• Cyclical Sectors Outperformed – Some of the best-performing sectors during the period for all indexes above were the cyclical sectors. These sectors are usually tied more closely to economic growth and tend to perform well when the economy is growing or expectations are improving. Cyclical sectors are characteristically some of the lower-yielding sectors, and indexes that select based on dividend yield are typically under-weight in these sectors compared to the broad market.

Diversifying for the Future

The recent rising rate environment has signaled an improving U.S. economic picture for some. If this is indeed the case and rates continue to increase, it could be beneficial to diversify dividend-paying equity exposure away from sectors that are most sensitive to rising interest rates and into sectors that could benefit from economic growth. This coincides with a broader exposure to more cyclical sectors (lower yield and higher dividend growth) and potentially less exposure to the more defensive (higher-yielding) sectors. To read more on this topic, please see the market insight we published here.

{kind=link}

1Source: Bloomberg

Jeremy Schwartz is director of research at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.