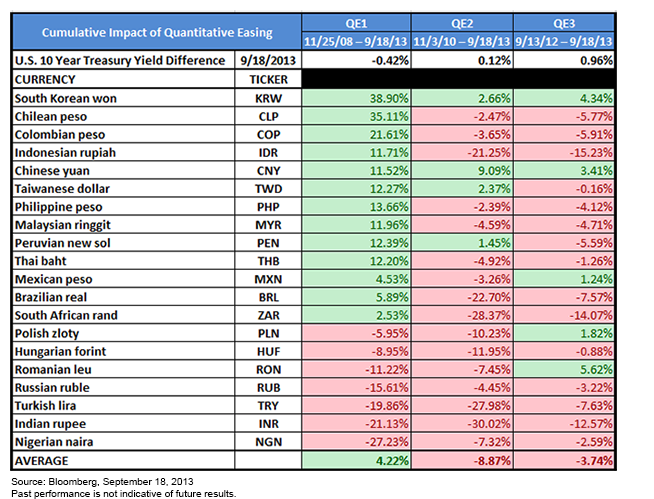

• Even after the Federal Reserve’s (Fed) recent policy surprise, 7 out of 20 emerging market (EM) currencies are trading at lower levels than before the Federal Reserve’s 1st quantitative easing announcement1

• While some countries face external headwinds, many EM countries were able to navigate the market volatility quite well

• With yields above 6.5%, EM local debt currently appears attractively priced on an absolute basis2

• On September 3, 2013, EM local debt was out-yielding U.S. high yield by the most significant margin in history3

• A pick up in Chinese economic momentum also offers a much firmer backdrop for the broader emerging markets

In part II of our series on investing in emerging market fixed income, we shift our focus from EM corporate debt to locally denominated fixed income, substituting currency risk for corporate credit risk in emerging markets. Although the market environment has proven particularly difficult—in fact, in the past five months local currency debt has generated the worst performance of all but one period in history—we believe that the most recent sell-off has created value in currencies as well as interest rates across many emerging markets. In light of recent guidance by the Federal Reserve, we believe that emerging markets could recapture an increasing percentage of investor flows and reverse the recent losses sparked by fears of “tapering”.

How We Got Here

After weaker economic data from key emerging markets disappointed investors, the law of unintended consequences reared its head due to comments by Federal Reserve Chairman Ben Bernanke. The possibility of a decline in the pace of Fed bond buying was cited as the primary catalyst for currency weakness and surging bond yields in emerging markets. Economies that once benefitted from foreign investor flows have underperformed since flows began to reverse.

However, we believe that those moves had overshot. With the recent FOMC meeting serving as a catalyst, we believe that locally denominated fixed income appears as an attractive way to play a less “hawkish” Fed.

{kind=link}

As shown in the table above, EM currencies, on average, are only modestly positive on a net basis since the depths of the global financial crisis. All told, the Federal Reserve has expanded its balance sheet by nearly $3 trillion; today, the U.S. dollar is stronger against seven out of twenty emerging market currencies. While we acknowledge that growth has slowed in many emerging markets as of late, we believe that current exchange rates do not accurately reflect the long-term potential of many of these economies. In many instances, EM currencies are now trading at multi-year lows against the U.S. dollar. Additionally, with only a single exception (the Chinese yuan), EM currencies continue to trade well off their high water marks set in 2006.

Next page: Emerging Market Interest Rates

Emerging Market Interest Rates

In a similar vein as EM currencies, EM interest rates appear attractive at current levels. As U.S. interest rates touched 3% for the first time in several years, EM rates approached the 7% mark for the first time in three years. At these levels, we believe that emerging markets currently strike an attractive balance between risk and reward. As compared to EM corporate credit, which has exposure to U.S. interest rates, investors in local debt are substituting currency risk (and volatility) plus local interest rate risk. As we noted in a recent blog post, we believe that once the market has acclimated to an eventual Fed tapering, emerging market interest rates will increasingly be influenced by domestic factors as opposed to U.S. policy. However, with rates rising significantly in advance of a Fed tapering that has yet to materialize, we believe EM assets are attractively priced.

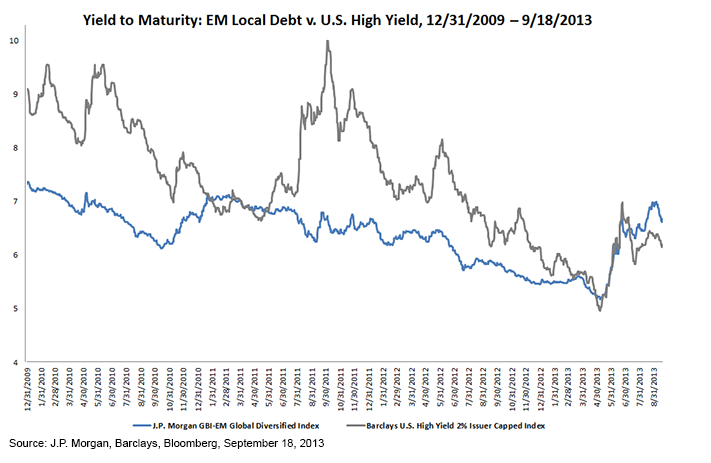

At present, the investable universe of emerging market local debt is rated 93% investment grade.4 With some emerging markets being upgraded as recently as May 2013, we believe that only a select few pose a risk of a credit rating downgrade. However, as shown in the graph below, EM local debt was recently offering the largest yield advantage compared to U.S. high yield in history.

{kind=link}

Compared to traditional U.S. Treasury Bonds, “opportunistic fixed income,” such as emerging market local debt, has a much different volatility profile. For many investors, investing in bonds with equity-like growth elements is a comparatively new undertaking. In light of recent market developments, we believe that volatility is going to be increasing for nearly all asset classes, including fixed income. However, there is a major distinction between volatility and solvency risk. The recent volatility in the asset class has largely been attributable to movements in emerging market currencies. But unlike past periods of rapid currency depreciation, emerging market economies have taken made significant strides to reduce their external vulnerabilities. At present, an overwhelming number of emerging market countries have significant levels of foreign exchange reserves. These reserves can either be converted from U.S. dollars to support/dampen the volatility of their exchange rates or be used to directly finance their government.

Outlook: Being Paid to Wait

Ultimately, we believe EM local debt is attractively priced at current levels. However, there is always the possibility that market volatility may persist as the U.S. struggles to provide appropriate guidance on the future path of interest rates. At current yields, we believe that EM local debt provides an attractive level of carry that may help dampen future volatility associated with locally denominated fixed income.

Rick Harper is head of fixed income and currency for WisdomTree Asset Management. This post was republished with permission from the WisdomTree blog.

1Source: Bloomberg, September 18, 2013

2Source: J.P. Morgan, Bloomberg, September 18, 2013

3Source: WisdomTree, J.P. Morgan, Bloomberg

4J.P. Morgan, August 31, 2013