If you typically review the first few paragraphs of conventional media reports, you might conclude that the United States is creating jobs at a torrid clip. Headline unemployment registered a 4 1/2 year low at 7.3%. What’s more, 169,000 positions in August sure sounds like a lot of new workers, doesn’t it?

The inconvenient truth of the matter is that true unemployment is at a 35-year high. Specifically the percentage of working-age individuals in the labor force hit a 1978 mark of a mere 63.2%. In other words, workers giving up the search for meaningful careers is the primary reason for the decline in the widely touted unemployment rate of 7.3%.

Sadly, the more one digs for answers, the more unpleasant the realities become. July’s 162,000 number was revised down to a meager 104,000; June was revised down from 188K to 172k, providing a 3-month rolling average of 148,000 positions. Keep in mind, in the 2003-2007 5-year span, an average closer to 200,000 had been described as a “jobless recovery.”

Honestly, I wish there were something more positive to say about the job growth. However, even the positions that are being added are largely at the lowest end of the earning spectrum and 70% of them are part-time. That’s right… part-time jobs count as gains in the headline 7.3% figure.

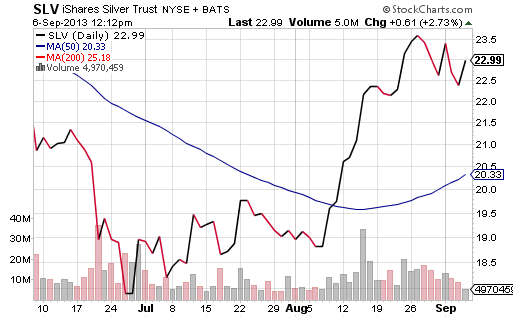

However, there may be a silver lining for investors… and I do mean silver. Precious metals ETFs like iShares Gold Trust (IAU), iShares Silver Trust (SLV) and PowerShares MultiSector Precious Metals (DBP) are keenly aware that the Fed is likely to hold off any significant tapering activity in September. These assets catapulted on the weakness of the employment data.

{kind=link}

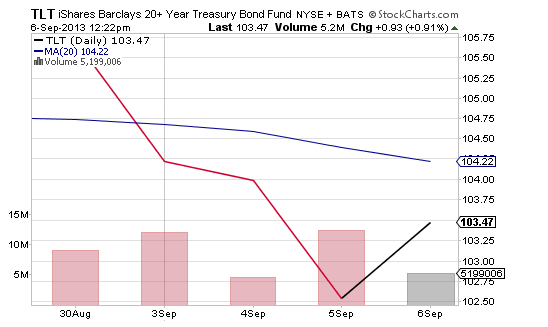

Granted, long treasury bonds as well as extended duration treasury bond ETFs could not buy a break since the Fed began hinting about slowing its bond purchases back in May. Even the threat of a military strike on Syria failed to lift income-oriented ETFs. With the Bureau of Labor Statistics (BLS) presenting its findings for August, though, funds like iShares 20 Year Treasury (TLT) smelled the possibility of a reversal.

{kind=link}

Perhaps ironically, the increasing unlikelihood of meaningful changes to Fed policy on September 18 is keeping stock investors engaged. (At least for now.) And why not? Quantitative easing (QE) may be subject to the law of diminishing returns, but returns there still are. Even the highest estimate of Fed “de facto tightening” of its QE3 policy is to slow the bond buying from $85 billion down to $65 billion; that’s still equivalent to the stimulus associated with QE2 — the same stimulus that is credited with 2nd half 2010 gains as well as 1st have 2011 success.

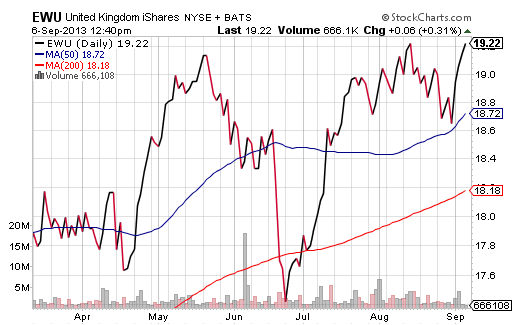

Of course, before getting giddy about the strong possibility of stateside stimulus, I must emphasize a preference for “steady-as-she-goes” foreign stimulus. For example, the Bank of England (BOE) has been making it real easy to like iShares United Kingdom (EWU).

{kind=link}

Gary Gordon is president of Pacific Park Financial, Inc.