As students around the country return to the classroom, it strikes me that now may be a good time to get back to the fundamentals on the municipal bond market as well.

The summer was a fairly tortuous one for the asset class, with the S&P Municipal Bond Index having lost 5.57% between June and August. In fact, most fixed income sectors struggled as interest rates spiked after the Federal Reserve’s first hints of easing off quantitative easing. Notably, the volatility in the muni market over the past few months has had a lot to do with rates — and very little to do with credit events (even big ones like Detroit).

Despite the volatility and headline noise, in my opinion, the reality is that the fundamentals underlying the municipal market are stronger than they have been in five years. A big statement? You bet. And here are just a few reasons to believe it:

State revenues have seen one direction — up. States have notched 13 consecutive quarters of rising tax collections, according to data from the Rockefeller Institute. Preliminary data for April and May indicates that a 14th quarter of improvement appears to be in the making. While revenues have increased, expenditures generally have been well contained as states continue to function with a level of fiscal discipline that had been passé prior to the 2008 financial crisis. The Institute notes that state and local governments trimmed more than 680,000 jobs since August 2008, and are likely to continue “doing more with less.” Higher revenues and lower expenditures is a fiscally powerful combination that has been leading to balanced budgets and increasing reserves nationwide.

Moody’s upgrades its outlook for states. Moody’s recently revised its outlook on US states to “stable” after five years at “negative.” In addition to citing improving revenues and reserves, the agency also noted in its announcement that credit quality among US states remains “extremely high,” with 30 of the 50 states having the two highest possible ratings. In fact, as I noted in my post “Three Pictures Paint the Big Picture in Muniland,” the municipal market overall is relatively high quality, with an average rating of AA as of year-end 2012.

Stronger housing = stronger locals. While the recovery across local governments trails that of states (Moody’s maintains its negative outlook for locals), we would point to strengthening housing prices as a promising omen for locals. Property taxes make up the lion’s share of local revenues and, as such, strength in housing bodes well for local governments. The National Association of Home Builders’ First American Improving Market Index found that 291 metropolitan areas across the country qualified as improving housing markets in September, a gain of 44 markets from one month prior.

Pension reform is gaining traction. It’s no secret that oversized pension burdens have been a drain on state and local governments. Even with improving stock markets, pension funded levels have languished. Ironically, the financial crisis brought the pension problem to the fore, and the hard work of addressing the issue has already begun. Between 2009 and 2011, 43 states enacted some sort of pension reform, according to the National Conference of State Legislatures. Detroit’s large pension burden added an exclamation point to the conversations, and may be the impetus for increased reform — and relief for overburdened municipalities. We cite the California city of San Bernardino as another potential precedent setter in our September market update, with some expecting an eventual Supreme Court decision before all is said and done. Ultimately, there seems to be a growing acknowledgement that achieving greater local budget flexibility will require a more aggressive approach to pension reform.

We are not Polyannas. We know the recent market correction has been painful for muni bond holders. The ugly truth, however, is that corrections are necessary. They restore value in the market and present the opportunity for investors to buy in at attractive levels — a new base from which your investment can grow. I think that is exactly what the market is doing here — recreating value from a point of very low, unsustainably low, interest rates.

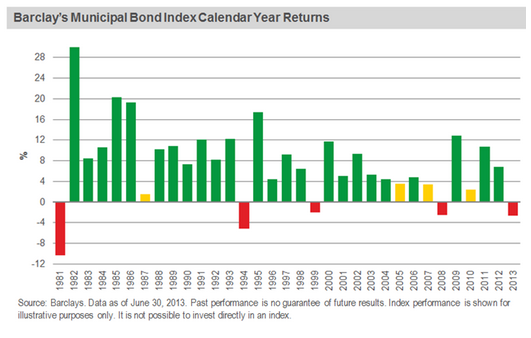

As illustrated in the chart below, over time, negative periods in the municipal market have been followed by boons. For those who are able to weather the near-term uncertainty, we think this may be a good time to capture muni exposure at levels not seen since 2011. The fundamentals in the overall municipal bond market are strong, and we believe the market will acknowledge that fact — and patient investors will be rewarded.

{kind=link}

Bonds and bond funds will decrease in value as interest rates rise and are subject to credit risk, which refers to the possibility that the debt issuers may not be able to make principal and interest payments or may have their debt downgraded by ratings agencies. A portion of a municipal bond fund’s income may be subject to federal or state income taxes or the alternative minimum tax. Capital gains, if any, are subject to capital gains tax.

Peter Hayes, Managing Director, is head of BlackRock’s Municipal Bonds Group.