My usual gig here on the blog is to report on ETF inflows and outflows, which is a great way to help investors identify emerging trends. Something that always strikes me is that if you only read my blog posts, you might get the impression that the categories I’m discussing (for example, broad US equity or high yield bonds) are the only ETFs seeing any trading action.

But with ETFs making up more than 25% of equity market trading volume most months, this simply isn’t the case.

The truth is, even funds that don’t have net inflows and outflows – or primary market activity – can still experience considerable secondary market trading volume. What’s more, the fact that they do is a great illustration of one of the most salient benefits of ETFs.

For many ETFs, significant two-way (buy and sell) activity generally means that investors can trade the fund back and forth without there being a need for creations and redemptions. The iShares Emerging Markets ETF (EEM) is a great example of this phenomenon. Because some of the fund’s underlying securities tend to be thinly traded and hard to access, EEM has become a preferred vehicle for trading these emerging markets stocks. As a result, it has grown very large (~$39 billion as of 9/11/13) and typically sees a lot of secondary market trading volume.

For example, between August 6th-13th (six consecutive trading days), EEM had no net inflows or outflows. Meanwhile, the fund’s average daily volume (ADV) during that time was $2.4 billion. Close to 360 million shares, or $14.2 billion, changed hands without any need to tap into primary market liquidity. That’s a lot of two-way volume.

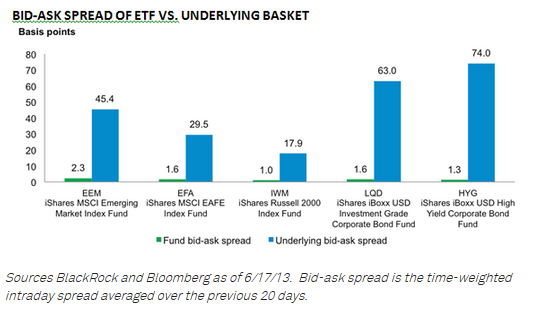

There are a couple of big takeaways for investors. Generally the more trading volume a security has, the tighter its bid-ask spread tends to be, which lowers the trading cost for investors. In some cases, the ETF’s spread is actually tighter than the spread of its underlying securities – this is typically the case with some of the more liquid ETFs out there (see below). For example, EEM’s spread of 2.3 basis points compares favorably to the average weighted bid-ask spread for its underlying basket of stocks at 45 basis points. That cost savings, for the same economic exposure, can be attractive to investors transacting in the secondary market and is a compelling feature that many ETFs offer.

{kind=link}

In addition to the benefits of secondary market liquidity, ETFs also benefit from the primary market function. When there’s significant supply or demand pressure on an ETF, shares can simply be redeemed or created in order to meet investor needs. This means that an ETF’s on-screen liquidity (i.e. shares available to trade) only tells part of the story, because authorized participants (APs) can always make more.

When we say that ETFs have “two layers of liquidity” or “hidden liquidity”, this is what we’re referring to: the secondary market, which can provide easier access and tighter spreads, and the primary market, which can meet the supply and demand needs of investors.

Dodd Kittsley, CFA, is the Head of Global ETP Market Trends Research for BlackRock.