Exchange traded funds offering exposure to emerging markets debt, both of the dollar-denominated and local currency varieties, are among this year’s most downtrodden funds. Spooked by increased borrowing costs for developing economies that lived off the fat of the Federal Reserve’s ultra-loose monetary policy, investors have not been shy about pulling cash from emerging markets bond funds.

Of the 10 worst ETFs in terms of year-to-date outflows, four are bond funds and one is the iShares J.P. Morgan USD Emerging Markets Bond ETF (NYSEArca: EMB), which has lost nearly $2.3 billion in assets since the start of the year. That is nearly triple the amount pulled from the PowerShares Emerging Markets Sovereign Debt Portfolio (NYSEArca: PCY). [A Splash of Kardashian for EM Bond ETFs]

There are signs the outflows trend is starting to reverse for developing world bond funds. For three straight weeks, emerging markets equity funds have seen positive flows and bond ETFs are finally getting a piece of that action. “For the week ending September 25, $0.56 billion, or 0.2% asset under management (AUM), went into EM bond funds. Hard currency funds benefited the most from the improved sentiment, seeing $0.37 billion, or 0.4% AUM, flowing in. Local currency bond funds turned the corner too, with $0.19 billion inflow,” Barron’s reported citing Barclays.

News of inflows, no matter how small, to emerging markets bond funds, is a departure from recent news pertaining to the asset class. Barclays data showed over $2 billion was pulled from emerging markets bonds ETFs during the last week of August, up from $1.3 billion in the prior week. [For the Brave, EM Bond ETFs Offer Opportunity]

Still, it could take more than just a week of inflows to convince all market observers that the time is right to reconsider developing world debt. Earlier this week, the Asian Development Bank expressed concern that easy access to credit is becoming more restricted and “the impact of higher interest rates on the economy may be intensifying” for countries in Emerging East Asia, a region that includes Hong Kong, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Thailand and Vietnam. [This Region Could be Problematic for EM Bond ETFs]

Others contend the outlook for Asian corporate bond issuance remains robust and that could benefit select ETFs.

“We see three main reasons for the dramatic growth in issuance – and, critically, despite recent market volatility, we expect all three to remain in force over the secular horizon. First, there is a lack of U.S.-dollar-denominated sovereign supply as countries develop, mature and increasingly prefer to issue debt in their own currencies. Second, we expect continued strong demand for spread product as net issuance globally remains at fractions of pre-crisis levels. Finally, post-crisis deleveraging within the banking sector has companies looking outside their traditional banking relationships for financing – and to satisfy their growing appetite for mergers and acquisitions overseas,” said PIMCO, the world’s largest bond manager, in a research note.

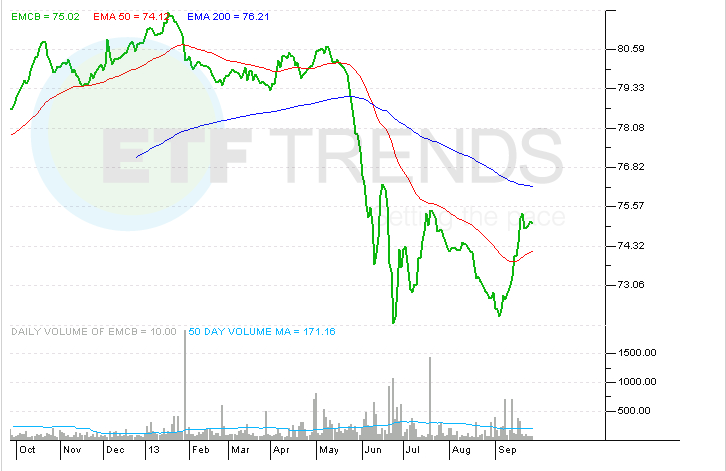

Improved sentiment toward emerging markets bonds, in particular corporates and quasi-sovereigns, should benefit an ETF like the WisdomTree Emerging Markets Corporate Bond Fund (NasdaqGS: EMCB). EMCB allocates almost 14% of its weight to Asian issuers.

WisdomTree Emerging Markets Corporate Bond Fund

{kind=link}

ETF Trends editorial team contributed to this post. Tom Lydon’s clients own shares of EMB.