Plenty of ETFs will potentially be affected by the expected tapering announcement at the end of the Federal Reserve’s two-day meeting later today, but any ETF with exposure to the mortgage bond market will be under even more intense scrutiny.

The Fed’s easing program has consisted of purchases of Treasuries and mortgage-backed securities. Tapering speculation has proven destructive for mortgage REIT ETFs like the iShares Mortgage Real Estate Capped ETF (NYSEArca: REM) and the Market Vectors Mortgage REIT ETF (NYSEArca: MORT). Those funds are down an average of 11.5% since May 22, the day tapering chatter truly escalated.

Since the end of the financial crisis, mREIT stocks and ETFs had been solid performers, getting a lift from the Federal Reserve’s ultra-loose monetary policy. Near-zero interest rates made financing cheap, allowing REM and MORT holdings to use leverage to bolster their yields. [Mortgage REIT ETFs Plundered by Rising Rates]

The Fed has been buying $40 billion in mortgage-backed securities per month, which had been a boon for MORT and REM, but rising Treasury yields have plagued these ETFs. Higher interest rates and tapering could do the same to mortgage-backed securities ETFs.

Mortgage-backed securities also are the most vulnerable to rising benchmark rates because the underlying loans aren’t likely to be refinanced as often. That leaves investors stuck with a low-return asset for a longer period than previously expected. [Mortgage REIT ETFs Hit by Fed Tapering Chatter]

Additionally, it is easy to see why the Fed needs to taper its mortgage-backed securities purchases. Common sense dictates $40 billion a month starts to add up. The growth of mortgage-backed securities on the Fed’s balance sheet was up to $1.246 trillion as of June 30, 2013, versus $950.321 billion as of December 31, 2012, according to 24/7 Wall Street. That is a 31.1% increase.

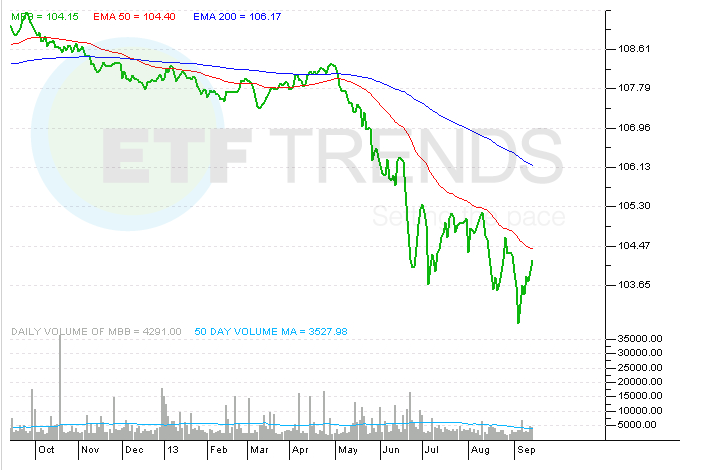

Reduced purchases of mortgage-backed securities could plague ETFs such as the iShares MBS ETF (NYSEArca: MBB). MBB provides exposure to U.S. agency mortgage-backed bonds, including Government National Mortgage Association (GNMA), Federal National Mortgage Association (FNMA) and Freddie Mac (FHLMC) securities, according to iShares.

Going forward, the tapering-fueled issue that could weigh on an ETF like MBB is the recent surge in mortgage rates. Higher mortgage rates are comparable to higher bond yields. The result is lower income due to lower coupons. “The trailing six-months of income from the MBS pools was $15.988 billion for the first half of 2013, versus $16.581 billion for the first half of 2012,” according to 24/7 Wall Street.

Accordingly, MBB is down 3.5% year-to-date and 2% in the past 90 days.

iShares MBS ETF

{kind=link}

ETF Trends editorial team contributed to this post. Tom Lydon’s clients own shares of REM.