U.S. equity markets have been strong thus far in 2013, and small-cap stocks particularly so. Recently, we have focused on the WisdomTree SmallCap Earnings Index, with particular emphasis on strong performance—a focus that we reiterate here.

When market movements reach this level, it’s important to ask whether these moves are justified in each case.

Are share prices moving more than their underlying fundamentals? A focus on valuation becomes increasingly important when equity markets move at such a speed.

Below, we will discuss the process the WisdomTree SmallCap Earnings Index employs to manage the valuation risk inherent in gains of nearly 38% over the prior year.

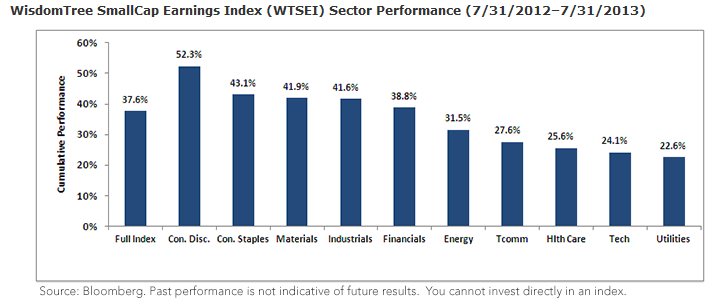

What we see (in this case on a sector basis) is that WTSEI delivered a nearly 38% return over the period, with strong returns spread across all 10 sectors, ranging from 22% at the low end for Utilities to over 52% at the high end for Consumer Discretionary stocks.

{kind=link}

• Consumer Staples and Cyclical Sectors Lead: The two Consumer sectors (Consumer Staples and Consumer Discretionary) lead the way within WTSEI over this period. Much has been made of the potential for the Federal Reserve to alter its policy due to a perceived strengthening of the U.S. economic picture. Other cyclical sectors—Materials, Industrials and Financials—also had returns of nearly 40% or more.

Are Valuations Getting Stretched?

Strong performance is well and good, but a potential issue with market capitalization-weighted indexes is that they tend to simply hold what has run up in price instead of rebalancing based on any metric of relative value. In essence, there is no mechanism employed with a disciplined regularity that attempts to shift weight from what has performed strongly in the past to what may have potential to perform strongly in the future.

How WTSEI Delivers a Disciplined Rebalancing Process

Every year on November 30, WisdomTree runs a screen upon which a subsequent rebalance of WTSEI is based. The purpose of this screening and rebalancing process is simple:

• Looking to trim weight from stock positions whose prices have appreciated significantly but whose fundamentals may not have increased commensurately.

• Looking to add weight to stock positions whose prices have stagnated or even fallen but whose fundamentals may have actually exhibited positive growth.

It is in this way that WisdomTree looks to mitigate the risk of being exposed to firms that may have enjoyed strong momentum and price increases but whose price levels may be at a relatively higher risk of being classified as “expensive.”

Continual Focus on the Earnings Stream

Mechanically, WTSEI’s rebalancing process is based on the Earnings Stream, which, simply put, is derived from a firm’s earnings per share multiplied by its number of shares outstanding. This ends up being much different than the process employed by market capitalization-weighted indexes, where the weights are determined by multiplying share price with the number of shares outstanding. In essence:

• WTSEI “rewards” (with greater weights) the firms that have generated the greatest levels of earnings.

• A market capitalization-weighted index “rewards” the firms with the greatest market capitalizations, which in many cases ends up being the firms whose share prices have increased the most.

Perhaps the most interesting element of WTSEI’s rebalance is the fact that each and every year companies must demonstrate profitability to maintain their eligibility for inclusion. Put another way: firms that on the screening date cannot demonstrate a prior four quarters of cumulative positive earnings are excluded from the Index.

Conclusion

After such strong performance in U.S. small-cap stocks, we believe a focus on a disciplined rebalancing process gains significant importance. While market capitalization-weighted indexes may simply continue giving the greatest weights to the firms with the largest market caps, WTSEI focuses on fundamentals, specifically the Earnings Stream, to determine its constituent weights. We believe this gives WTSEI the potential to sell stocks that have become more expensive and buy stocks that have become less expensive relative to the earnings they have generated. In essence, this could be one way to manage risk after a market rally.

Christopher Gannatti is a research analyst at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.