The recent rally in Russian equities is testimony to the ability of its local markets to thrive in an environment of rising U.S. bond yields. With an encouraging second-quarter gross domestic product (GDP) out of the U.S. and a sanguine July Federal Open Market Committee (FOMC) outlook, markets are widely anticipating tapering to occur as early as the fourth quarter this year. While policy rates will remain accommodative for a longer period, steady improvements in the U.S. economy may result in a further increase in treasury yields.

On a relative basis, this may position Russia to perform better than its emerging market peers. From a macroeconomic perspective, Russia has a healthy current account surplus of 2.6% and is thus less dependent on foreign inflows. Many emerging market nations, such as India, South Africa and Indonesia, run large current account deficits and rely on foreign inflows to fund them.

Russia’s current account surplus is especially important in a time of rising U.S. yields. The EM block has experienced outflows, partly due to the narrowing yield gap between the U.S. and the rest of the emerging markets. The closing of this gap renders the EM block less compelling from a yield perspective. However, we feel that Russia is well positioned to withstand the storm, as it is less reliant on external funding and thus better able to keep its monetary policy loose (i.e., low interest rates), while other EM nations tighten their monetary policy—which can slow down their economies—in order to attract foreign flows.

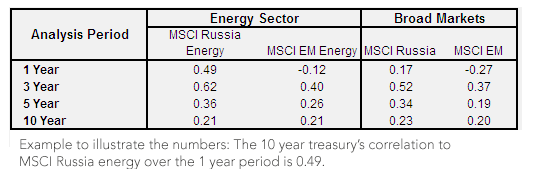

Further, we find that Russia’s equity markets—and the energy sector in particular—are positively correlated with U.S. interest rates3 (10-year yields).

• Emerging market stocks have been positively correlated to U.S. interest rates over longer periods (three, five and ten years), but Russian stocks have been more positively correlated.

• While emerging market stocks were negatively correlated to U.S. 10-year yields over the last one-year period, Russian stocks (and especially Russian energy stocks) were positively correlated over the same period.

• Given that roughly 50% of Russia’s market is composed of energy stocks, it is not surprising that the overall Russian markets exhibit positive correlations to bond yields.

• The positive correlation between Russian energy sector and interest rates seems to be explained by a connection between higher interest rates and stronger global economic growth, which is supportive of energy prices and the Russian markets.

Table 2: Russian Stocks Display Higher Correlation to 10-Year Bond Yields Than MSCI Emerging Markets4

{kind=link}