Japanese stocks have soared since Shinzo Abe was elected prime minister based on the belief that his “Abenomics” policies will reinvigorate Japan. All of Abenomics’ goals are aimed at one thing: promoting economic growth in Japan.

A Depreciating Yen Helps Japanese Large Caps

Thus far, Abenomics has coincided with a weaker yen, which has helped large multinational companies that sell products overseas. Products of these companies generally become more attractive to foreign buyers when the yen weakens. Also, overseas sales converted back to a weak yen translate to more yen revenue, ultimately adding to the bottom line.

Domestic Consumption Is the Government’s Larger Focus

However, at its core, Abenomics is designed to stimulate economic growth in Japan—by encouraging Japanese consumers to come off the sidelines. Monetary policy provided an initial positive jolt, but more structural reforms are needed. Abe is still working on these structural reforms—and I expect more will be done this year. I believe we may just be in the early innings of renewed growth in local consumer demand.

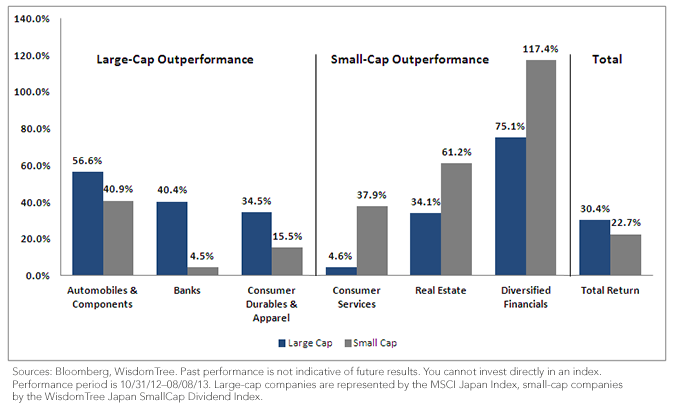

Return Differences among Large Caps and Small Caps

Small caps are often more sensitive to the local economy than large caps. Below I contrast the difference in performance between Japanese large caps and small caps by comparing the MSCI Japan Index to the WisdomTree Japan SmallCap Dividend Index. The MSCI Japan Index represents the largest-market capitalization firms in Japan, while the WisdomTree Japan SmallCap Dividend Index represents smaller-capitalization, dividend-oriented firms. Although there are vast performance differences among the many industry groups, small caps as a whole have lagged large caps over the period shown below.

Industry Group Performance

{kind=link}

• Large-Cap Banks Outperform – The largest-cap banks, such as Mitsubishi UFJ Financial Group, Mizuho Financial Group and Mitsui Financial Group, are all up over 40% during the period. These three banks have profited more from a weaker yen and a rising equity market than some of their smaller counterparts. They have benefited from increased capital market activity, investment trust sales and brokerage fee income, all of which continues to grow with the stock market recovery.

• Small-Cap Real Estate and Diversified Financials Outperform on Domestic Trends – Real estate companies and real estate investment trusts (REITs) have been among the strongest performers. The Bank of Japan has been buying REITs, which has provided a tailwind for the industry.

• Automobiles and Consumer Durables Increase on Yen Weakness – Large automakers such as Nissan, Honda, Mazda and Toyota have all benefited from a weakening yen due to their export-oriented business models. Yen weakness has accounted for a majority of the automakers’ recent profitability, and Toyota just announced that ¥260 billion of their approximately ¥270 billion profit could be attributed to yen weakness.1 Consumer durables companies such as Sony and Panasonic have also benefited from a weakening yen, essentially making their products more attractive to overseas customers and boosting foreign profits through a lower, more advantageous exchange rate.

• Consumer Services Tied to Local Economy – The large performance difference in the consumer services industry is mainly a result of the industry group composition. A majority of these firms are tied to the local economy. As consumer confidence continues to increase, I expect this industry group to continue to benefit.