Dennis Lockhart is a non-voting member of the Federal Reserve’s monetary policy committee, yet his opinions can still move stock markets.

On Tuesday (8/7/2013), stocks pulled back because Mr. Lockhart suggested that the Fed may indeed slow its bond buying program as early as September. One of the main criteria? Job creation in August would need to rise from July’s 162,000 to 180,000-plus.

Let me be politically incorrect here for the moment. Do the smartest individuals in the country genuinely feel that an extra 13,500 part-time, entry-level positions in August would signal robust job growth? Three-fourths of the net new jobs in 2013 are part-time and most of those are at the lowest end of the wage scale (e.g., hospitality, retail, etc.). In other words, if all Dennis Lockhart needs to see is 18,000 more jobs than he witnessed in July, then he favors tapering the Fed’s bond program with 13,500 additional part-timers.

Perhaps policymakers and influential speakers simply wish to curtail emergency level stimulus sooner so that there’d be more wiggle room. Over the last 5 years, we’ve seen QE1, QE2, “Operation Twist” and QE3. Each time that one program has neared its completion, the Fed eventually trotted out another rate-manipulating project. It follows that if the housing recovery reversed course, or if the U.S. stock market found itself in the midst of a 15%-20% volatile correction, we should expect the Fed to go for a fourth round of quantitative easing (a la “QE4″).

Still, even if the Fed consistently comes to the stock market’s rescue, investors may be ignoring critical warning signs. For example, most of the hype surrounding hedge fund manager Jim Chanos has centered on his China bearishness. Less commonly discussed? Chanos has pointed out that there are more stocks with price-to-book (P/B) ratios above 3.0 today than there were in 2000.

Could U.S. stocks be this wildly overvalued? That depends upon who you ask. Moreover, the price-to-book phenomenon primarily reveals that small-cap shares were far cheaper in 2000 or, at the very least, valued much differently back then. Large-cap stocks are not quite as overextended.

Even if you prefer price-to-earnings ratios, Birinyi Associates peg the large-cap barometer (S&P 500) at 18.6. The small-cap barometer (Russell 2000) is sitting on a trailing price-to-earnings ratio of 48.9. Only by accepting forward 12-month estimates for the Russell 2000 do you get to a more tolerable 18.8.

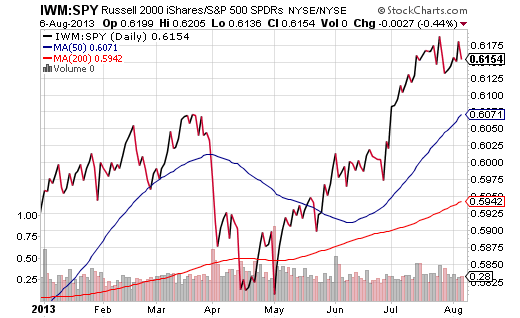

For those who are less inclined to take valuations as seriously in this Fed-fueled rally, there are relative strength indications to consider. The iShares Russell 2000 (NYSEArca: IWM) is the strongest that it has been relative to the S&P 500 SPDR Trust (NYSEArca: SPY) all year.

I am not suggesting that ETF enthusiasts stampede for the exits and sell all of their small-cap stock holdings. By the same token, even a momentum buyer may wish to tread lightly in the small company arena.

{kind=link}

Gary Gordon is president of Pacific Park Financial, Inc.