With abnormally low yields over the last few years, investors have been on high alert to the potential impact that an unpleasant end to a 30-plus year bull-run in bonds could have on their portfolios.

With US 10-Year Treasury yields rising over 80bps since the end of April, many investors are now feeling the pain. While other asset classes may offer greater potential for risk-adjusted returns in today’s market, fixed income can and should remain core to investment portfolios due to its potential for income generation, diversification and capital preservation. Fortunately, there are opportunities available for savvy investors to create resilient portfolios regardless of how far and fast rates may rise over the rest of the year.

Bonds under pressure

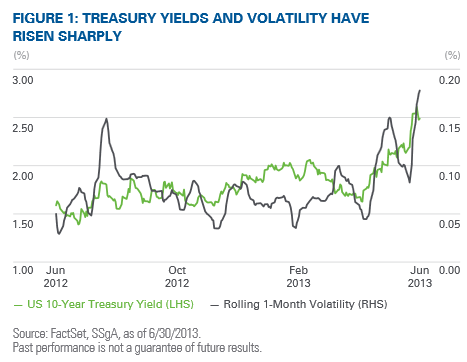

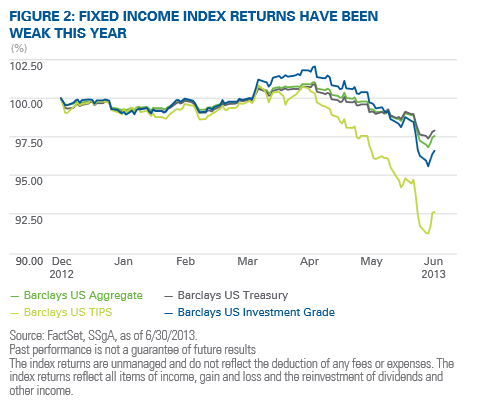

As the economy continues to recover from the Great Recession and the lingering impacts of the European sovereign debt crisis subside, it comes as no surprise to see rates on the rise. What seems to have caught investors by surprise however, is the speed at which rates moved after Fed Chairman Ben Bernanke suggested that QE may be tapered off sooner than consensus expected. As highlighted in Figure 1, US 10-Year Treasury yields have spiked over the last two months, which introduced greater volatility into the fixed income market. This move has led to negative returns from various segments of the fixed income market as shown in Figure 2.

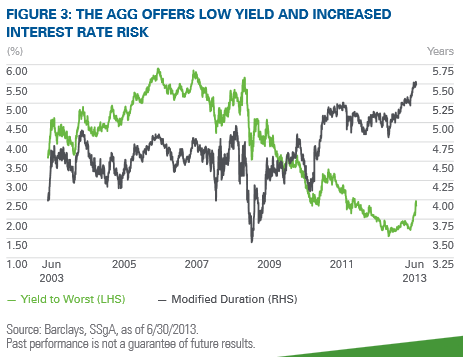

For investors looking for core exposure to the fixed income market, the Barclays US Aggregate Index (Agg) has been the traditional vehicle of choice. Even after not faring well year-to-date, the Agg offers investors a relatively low yield with increased interest rate risks relative to history, as illustrated by the divergence in yield and duration shown in Figure 3. What is driving this potentially detrimental change? One factor is that the weight of Treasuries in the Agg has increased over the past five years. In isolation, this is not necessarily bad. However, what is disconcerting is that the Agg’s increase in duration can be attributed to the rise in Treasury exposure.

Skeptics may counter with “so what”? The Agg is simply reflecting the US investment grade market as it always has. Exposures will ebb and flow over time. While technically correct, this thinking may add to the risk inherent in today’s market. Fortunately, investors no longer need to think simply about core exposure or core plus to meet their investment needs. Many have already begun to integrate the next generation of fixed income into portfolios on a more consistent basis. Taking this a step further with greater control over exposures will allow for further precision. In other words, investors no longer need to think of allocations across bond market sectors as merely a bolt-on approach.

Solutions for rising rates in today’s market

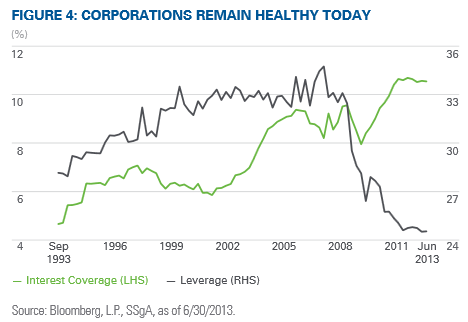

With corporations maintaining a focus on balance sheet management, firms remain generally healthy today. Leverage ratios are moderate and interest coverage is strong as highlighted in Figure 4. While global economic risks remain slightly skewed to the downside, corporations are benefitting from an environment of improving economic growth with low inflationary pressures. At the same time, a rising US dollar in the near-term may help drive increased consumption, adding further fuel to the tailwinds of a housing recovery and better jobs numbers. Thus, investors should feel comfortable taking on credit risk to meet their income needs. In addition, default rates are expected to remain low over the coming year. By diversifying portfolios across fixed and floating rate investment-grade high-yield securities, investors will be able to construct portfolios that meet their needs in an environment of rising rates.

Next page: Short-term corporate bonds

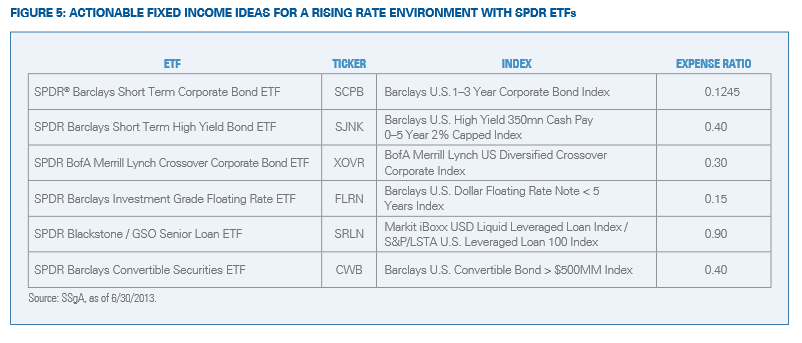

Short-term corporate bonds

In today’s market, a main concern for investors is interest rate risk. Shorter durations allow for greater protection in an environment of rising rates and for reinvestment at potentially higher yields. However, many investors may not be fully harnessing the credit exposure that they wish to target. More specifically, investors may wish to avoid exposure to the government-related sector as opposed to simply owning securities in the industrial, utility and financial sectors. What further compounds the matter is that government-related sectors are either highly leveraged or low yielding.

Short-term high yield bonds

Market participants have embraced the benefits of high yield bonds in a low rate environment and one conducive to credit exposure. With absolute yields compressed and option-adjusted spreads around historical averages, some are questioning how much more return the segment can provide. It may be the case that investors are correct to recalibrate their return assumptions, but the market is not yet exhibiting signs of excess froth from a credit perspective. While certain segments may be richly valued and subject to greater volatility, there are options for investors who wish to remain exposed to below investment grade credits, but with less potential for performance fluctuations. One such area is short-duration high yield. While high yield is a market segment with generally low duration, short-term higher yield offers attractive yield per unit of duration. The 0–5 year maturity window offers half of the interest rate risk of longer maturity bonds with the added benefit of less performance volatility.

Crossover bonds

By focusing on the lowest rated investment grade and the highest rated below investment grade crossover bonds, investors are able to harness inefficiencies in the corporate market. By doing so, investors can avoid the lower spreads available in higher rated AAA and AA-rated bonds while at the same time avoiding the most speculative, equity-like exposure of CCC-rated high yield bonds. In addition, what investors may not know is that BBB and BB-rated bonds have offered the highest sharpe ratios of any rating bucket over long-term periods.This market segment provides a relatively attractive yield with moderate duration, an excellent combination to combat today’s challenges.

Senior secured loans

With yields that are comparable to unsecured fixed rate high yield bonds, senior secured loans are an increasingly compelling option to further evolve portfolios in today’s environment. Senior loans are floating rate instruments while most high yield bonds are fixed rate. This means that loans have the ability to see their rate of income increase should rates normalize, which fixed rate bonds cannot do. More specifically, because loans reset they have minimal duration risk. Investors are increasingly recognizing that it pays to wait with loans. In addition, because loans are senior in the capital structure to bonds, they have experienced significantly greater recoveries in cases of defaults than have unsecured bonds.

Convertible securities

As hybrid securities, convertible securities combine the upside potential of stocks while exhibiting some of the downside protection inherent in bonds. Convertibles tend to have low sensitivity to interest rate risks, which make them more resilient to rising rate environments. In fact, while convertibles do pay interest they can be converted into their shares of the issuing company and have exposure to underlying equity fundamentals, which often perform well when rates are increasing.

Conclusion

With 10-year TIPS moving into positive territory, investors appear to be pricing in Fed tightening or at least tapering sooner than many expected. In fact, yields could move up more if economic growth surprises to the upside or the market continues pricing in Fed policy changes earlier than expected. Many are looking back to previous Fed tightening signals for clues and courses of action. With 1994 and 2004 potentially providing weak guidance due to the extent of extraordinary monetary policy today, investors should look beyond the core to build portfolios that behave less like return-free risk. In doing so, investors can also move beyond certain well-trodden segments that may be crowded and no longer offer their historical value propositions. Unique credit exposures through various corporate bond segments are an especially attractive solution today and allow for the development of more resilient and adaptive fixed income portfolios in a rising rate environment.

David Mazza is vice president and head of ETF investment strategy, Americas, for State Street Global Advisors, which manages the SPDR ETFs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}