Master limited partnership exchange traded funds provide investors with robust yields and exposure to the expanding energy infrastructure. However, MLPs could begin to struggle when interest rates move higher.

“Should interest rates begin to rise again, the cost of capital for MLPs would increase, which could result in lower distributions,” according to Morningstar analyst Abby Woodham. “MLPs have historically struggled during rising rate markets, but not to the extent of other rate-sensitive investments like REITs or high-yield fixed income.” [MLP ETFs: High Yield and Low Volatility]

Historically, MLP yields have relatively mirrored Treasury yield movements, with the exception of the financial crisis of 2008, writes Ingrid Pan for Market Realist.

Interest rates have an inverse relationship with bond and MLP prices. As yields rise, MLP valuations, like bond prices, typically decrease.

MLPs have attracted income-oriented investors during the “hunt for yield” as Treasury yields hit record lows.

Currently, benchmark yields on 10-year Treasuries are hovering around 2.6% after touching a 1.6% low earlier this year. The bond market saw yields move toward a 30 year low, and many market observers are anticipating a reversal to the three decade long bond rally. [An Equal-Weight ETF Approach to MLPs]

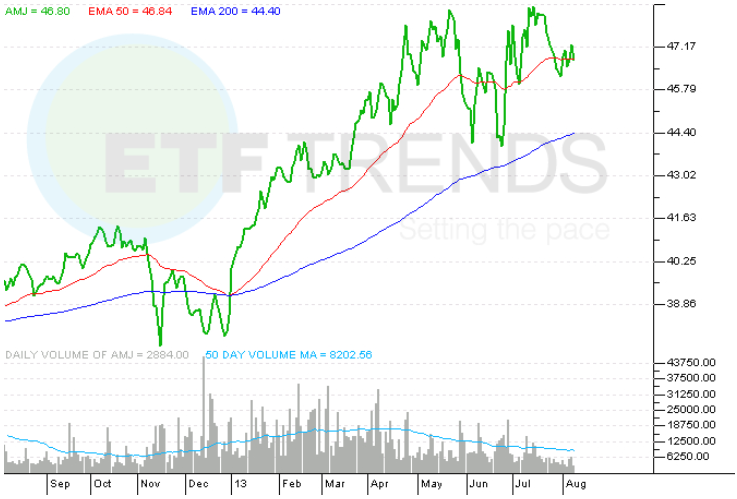

If interest rates inch up, MLP ETPs like the JPMorgan Alerian MLP Index ETN (NSYEArca: AMJ) or the ALPS Alerian MLP ETF (NYSEArca: AMLP) could begin to falter. AMJ is down 1.6% over the past month and gained 24.5% year-to-date. AMJ has a 4.56% 12-month yield and a 0.85% expense ratio. AMLP is down 0.7% over the past month and rose 14.9% year-to-date. AMLP has a 5.79% 12-month yield and a 0.85% expense ratio.[A Closer Look at Master Limited Partnership ETFs and ETNs]

JPMorgan Alerian MLP Index ETN

{kind=link}

For more information on master limited partnerships, visit our MLPs category.

Max Chen contributed to this article.

Full disclosure: Tom Lydon’s clients own AMLP.