London Bullion Market Association (LBMA) gold forward offered rates (GOFO) rates have now been negative for over 7 weeks. While GOFO rates have been negative during a few exceptional periods in the past, this is the first time they have been negative for a prolonged period, indicating tightness in the physical market for gold traded on the LBMA.

Strong demand from Asia and developing countries’ central banks, coupled with reduced supply from gold recycling and diminished mining supply, appear to have substantially tightened the market.

What are GOFO Rates?

Gold forward offered rates are effectively the interest an investor has to pay on gold-collateralized US dollar loans. Under normal circumstances, the GOFO rate is positive, with an investor having to pay interest to borrow US dollars against gold collateral. However, since the beginning of July 2013, the one-month and three-month GOFO rates have turned negative, meaning that an investor with gold is now being paid interest to provide gold as collateral against US dollar loans. It is worth noting that over the past week, gold forward rates have trended back into positive territory as higher lease rates (LIBOR – GOFO) have made it more attractive for central banks to lend gold into the market. Despite this, the gold physical market remains tighter compared to history.

Why Are GOFO Rates Negative?

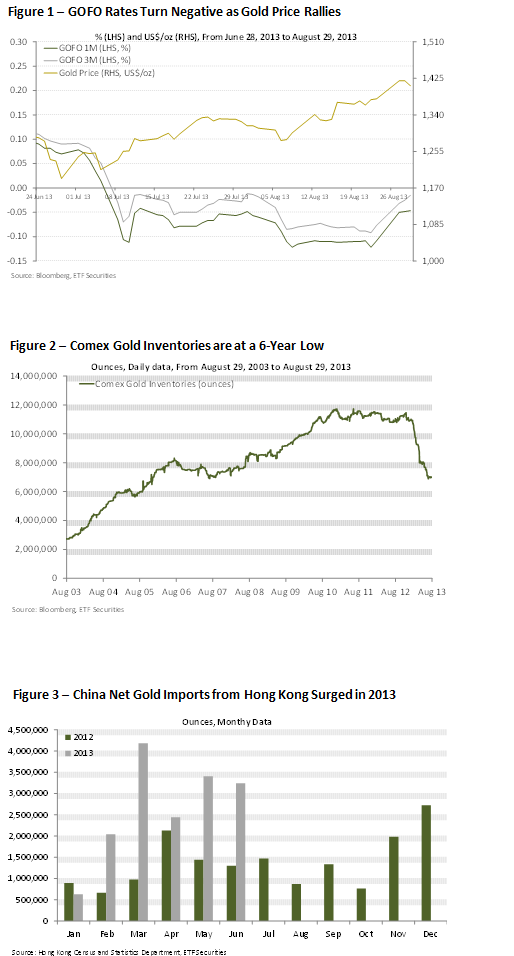

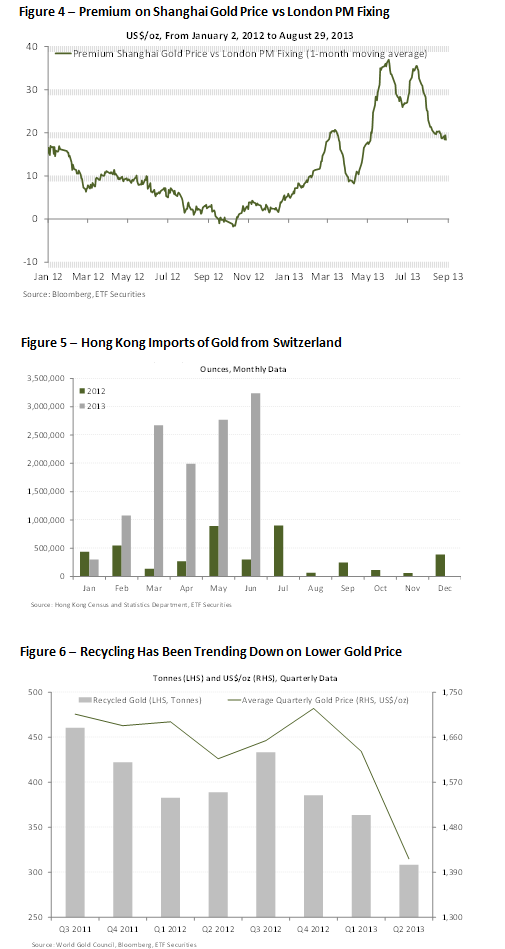

The most likely reason behind prolonged negative GOFO rates is a gold supply shortage. This appears to be confirmed by the simultaneous upswing in the gold price since July 2013 (Figure 1) and the sharp fall to a six-year low of gold inventories backing Comex gold futures (Figure 2). Since the slump of the gold price in mid-April, Comex gold inventories have fallen by 24%, highlighting the lack of liquidity in the gold forward market at the moment.

What Is Behind the Physical Gold Shortage?

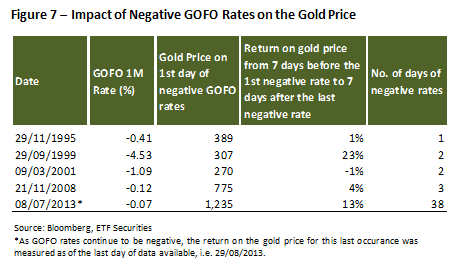

There are a number of factors behind the physical gold market shortage. First, the surge of China demand since early 2013. China imports of gold from Hong Kong in the first six months of 2013 amounted to 16moz, more than double the amount imported by China over the same period last year (Figure 3). Strong demand from China is also reflected in the premium of the Shanghai gold price over the London price (Figure 4). The premium reached a 21-month high in May. Despite the recent sell-off in the gold ETP market, physical buyers, particularly from Asia, appear to be taking up the slack. In the first half of 2013, UK exports of gold to Switzerland soared to almost 26moz, equivalent to 30% of global mine production, with much of the supply likely coming from ETF liquidations. Hong Kong imports of gold from Switzerland surged to 12moz over the same period, evidencing a shift in gold demand from the West to the East (Figure 5). The sharp fall in gold recycling is also likely weighing on overall physical availability, exacerbating the current shortage. Historically, there is a positive correlation between the gold price and scrap supply, as there is an incentive for gold holders to sell their gold when prices are elevated (Figure 6). Last year, 36% of gold supply came from old scrap as prices averaged US$1,669oz vs only 30% in Q2 2013 when prices averaged US$1,415oz.

Implications for the Gold Market

Historically, when GOFO rates have turned negative the gold price has also risen (Figure 7). With the exception of 2001, the gold price has tended to rally after the one-month GOFO rate has turned negative. Since July 2013, the gold price has increased by over 13% as a surge in physical buying following the April slump in price have drained liquidity out of the gold forward market. Imports of gold from China were 150% higher in June compared to the same period last year, continuing the trend of the previous months (Figure 3). Central bank buying also increased in the six months to June 2013, reaching 5.7moz, an 8% year-on-year gain. With demand from Asia and the official sector continuing to show strength, and recycling trending down, lack of liquidity in the gold forward market is likely to continue to support the gold price. In the longer term, with mine supply also likely to fall as gold miners struggle with rising costs and lower profitability, supply-side factors are likely to continue to support the gold price.

{kind=link}

{kind=link}

{kind=link}