Even before we buy our very first share of stock, we find ourselves riding the rails of an emotional roller coaster. Hope, anxiety, relief, denial, optimism, despair, euphoria, panic — these are the feelings that every investor experiences in a lifetime.

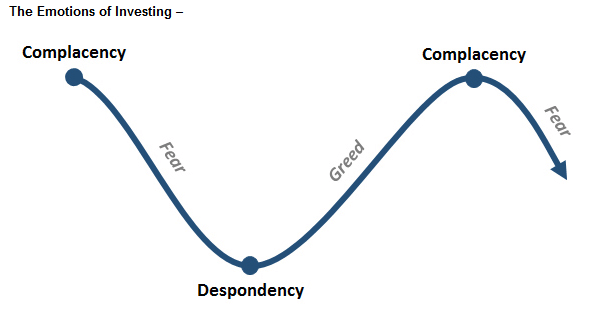

Emotions can generally be grouped into one of two categories: fear-based emotions and greed-based emotions. Fear-based emotions are most prevalent when markets trend downward. Complacency turns to anxiety, shifts toward denial, moves into despair and culminates in panic. Typically, it is near this point when investors take huge losses… when hope no longer springs eternal and despondency sets in.

As markets begin an inevitable rebound, greed-based emotions take hold of an investor’s psyche. Despondency turns to hope, swings to relief, moves toward optimism and cruises straight for euphoria. The hopeless memories have faded and the false comfort of complacency establishes a home. Alas, investors feel they can invest safely again, though it ends up being an exceptionally ill-timed decision.

What can one do about the emotional roller coaster? How can you avoid becoming your own worst enemy?

The first step is to recognize where your investment decisions begin. If you are like most investors, you envision, even fantasize about, how much money you are going to make. Any distant thought of selling your position hinges on how far “in the black” you are before you would ever think about ringing the cash register.

{kind=link}

But what if your investment doesn’t make it far enough into the black? What if it falls into the red? Heck… what if it never makes it out of the red? Do you have a plan to protect yourself in the event things don’t pan out? How bad must it get before you finally do something?

The problem most investors have is that they are extremely biased when considering both positive and negative outcomes. After all, if there were an equal likelihood that you could lose money on an investment, you might not purchase it at all, right? Few consider a 50/50 gamble to be advantageous to an investment portfolio.

A giant step in the right direction is realizing that successful investing has little to do with the odds of being right or wrong. Rather, it’s how bad you allow those wrongs to be.

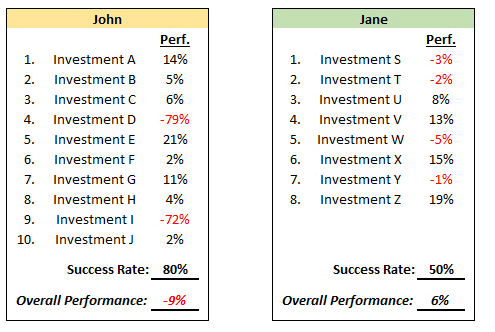

Consider the following example:

There are two money managers that have been in the business for over a decade. You are looking to hire one of them. John, runs a decent-sized hedge fund where he has made a total of 10 equally-weighted investments over the past year. Of those 10 investments, only 2 did not go his way. With his 80% success rate, John seems to have the ability to deliver excellent odds for moving your portfolio forward.

Jane, on the other hand, runs a small advisory firm. Jane made a total of 8 equally-weighted investments over the past year. Of those 8 investments, 4 of them did not go her way. With only a 50% success rate, Jane does not seem to offer any more value than a monkey throwing darts, right?

So who is the better money manager? Well, it depends.

In the example below, John only had 2 losing trades, but they were doozies. By letting just a couple of his investments get away from him, John’s overall performance was drastically affected. Jane, on the other hand, was far less successful than John at being able to pick winners; however, unlike John, she did not let any of her investments get away from her. When Jane was wrong on her selections, she sold them for small losses before they could negatively affect the larger portfolio. By doing so, she was able to significantly outperform John, even with a 50% success rate.

{kind=link}

The main lesson here is that avoiding the big loss is the key to overall performance. The best money managers understand that, when they are wrong, they must make certain they are only a little bit wrong. You cannot afford to be married to any of your positions. Pride, ego, product devotion, taxes, media hype – these are just excuses. Jane sees the big picture; John does not.

John may actually be bona fide genius. In fact, his reasons for initially choosing the two big losers above may have been nothing short of brilliant… so much so, that only an idiot would fail to see his logic. Unfortunately for John (and every investor), the stock market does not have to behave logically. Even a “guru” like John needs a discipline for selling.

Investors like Jane realize that the only bad investments are the ones you let get away from you. Establishing unemotional plans to limit your losses are just as important as the research you do to choose your investments.

Gary Gordon is president of Pacific Park Financial, Inc.