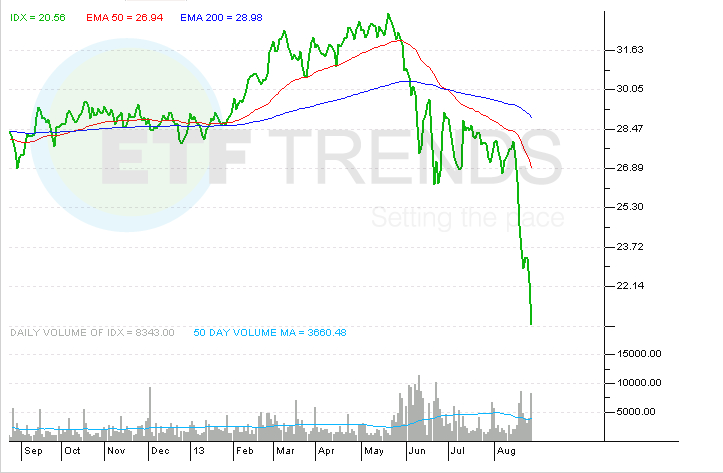

Exchange traded funds tracking Indonesia, Southeast Asia’s largest economy, have been at the epicenter of the recent emerging markets tumble. In just the past five U.S. trading sessions, the iShares MSCI Indonesia ETF (NYSEArca: EIDO) has plunged 14.3% while the rival Market Vectors Indonesia ETF (NYSE: IDX) is off 12%.

Indonesian ETFs have been hit by inflation worries, a widening current account deficit and expectations the Federal Reserve will taper its bond purchases. The declines are so severe that the new lows being set by IDX and EIDO are not just new 52-week lows. IDX, the older of the two ETFs, closed at $20.56 Tuesday, its lowest closing price since the fourth quarter of 2009. EIDO closed at $21.14, or 11 cents below its May 17, 2010 closing price. [Indonesia ETFs Lead Global Sell-Off]

But even with those staggering declines, Indonesian stocks and the aforementioned ETFs still are not sporting a trait shared by so many emerging equity markets and ETFs these days: Low valuations.

“The JCI [Jakarta Stock Exchange Composite Index] is currently trading at the lower end of its historical valuation (3.5x P/B). We note that the valuation of the JCI is not yet as cheap as during the 2008-09 global financial crisis (2x P/B), but the macroeconomic conditions and market sentiment are not nearly as bad as well. Commodity prices are still above the 2008-09 lows and global macroeconomic risks are much less now than then,” according to a Nomura note posted by Barron’s.

Other data points exist to support the notion that Indonesian stocks still are not as deeply discounted as markets such as China or South Korea. At the end of July, the MSCI Indonesia Index had a P/E ratio of 16.9 compared to 11.3 for the MSCI Emerging Markets Index, according to WisdomTree data. In fact, that P/E for the MSCI Indonesia Index was well above the 14.3 10-year average, the WisdomTree data show.

If 10-year Treasury yields continue rising, IDX and EIDO could be vulnerable to more downside. J.P. Morgan “is concerned that Indonesian equity performance, despite a 23% decline from the peak, has not reflected the risk of a structural increase in the country’s risk-free rates or decrease in its growth prospects,” reports Sulli Ren for Barron’s.

The ETFs are vulnerable on another front. Indonesia’s central bank has had to raise interest rates in an effort to support the rupiah. Those higher rates are could crimp loan growth, which is not good for news for EIDO and IDX given the ETFs’ weights of 34.1% and 34% to the financial services sector.

Market Vectors Indonesia ETF

{kind=link}

ETF Trends editorial team contributed to this post.