Over the last few weeks, there have been an inordinate number of articles concerning the high probability of a stock market crash.

One theory is that the super-sized year-to-date gains of the Dow coupled with the summertime interest rate spike is analogous to what transpired prior to Black Monday on October 19, 1987.

Another premise for a miserable September regards the fact that price-to-earnings (P/E) ratios are growing faster than at any time since the dot-come bubble burst in March of 2000.

Last, but hardly least, margin debt is at its highest level since the 2007-2008 financial meltdown.

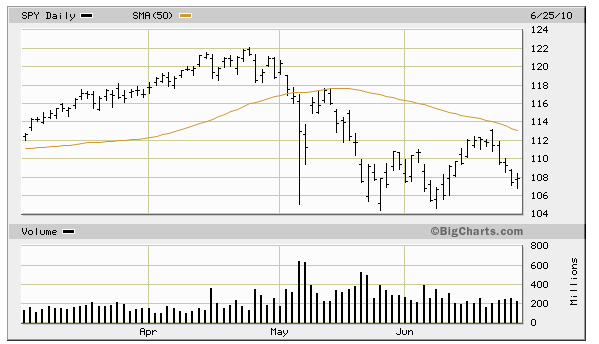

Of course, why should commentators stop at these comparisons? Our country’s M2 Money Supply as measured by currency in circulation as well as short-term deposits at banks appears to be slowing in the same manner as it did prior to the “October 1929 Crash.” What’s more, the S&P 500 SPDR Trust (SPY) is hanging around its 50-day moving average; the infamous “Flash Crash” in May of 2010 happened just as SPY had failed to maintain support at its 50-day trendline.

{kind=link}

Granted, I am being a tad bit facetious with my commentary. I do not subscribe to the notion that one can predict when a genuine crash will occur. Nevertheless, I acknowledge that there is no shortage of reasons to be wary. Institutional investors have been selling into August strength, Federal Reserve tapering uncertainty is serving to slow more than the rate of bond purchases and we’re once again bumping up against another debt ceiling debate.

For many of my client portfolios, we are maintaining a commitment to funds like SPDR Select Health Care (XLV), PowerShares Pharmaceuticals (PJP) and iShares DJ Aerospace and Defense (ITA). These ETFs have enviable defensive attributes where performance does not rely on an interest rate addiction nor economic cycles. They are hardly immune to sell-offs, pullbacks and crashes, but they do have staying power. (I’d consider buying more in a downturn.)

While I expect September to be weak for stocks due to a wide variety of economic, political and fundamental headwinds, those who believe a stock crash is imminent might consider one or more “reversal ETFs.” Specifically, the yen via CurrencyShares Yen Trust (FXY) could strengthen in a reversal of the carry trade, volatility via iPath S&P 500 VIX Short-Term (VXX) could rocket in a reversal of the complacency trend and extended duration Treasuries via Vanguard Extended Duration (EDV) could surge on a reversal of the “rates-can-only-go-up” thinking.

Gary Gordon is president of Pacific Park Financial, Inc.