Few asset classes have proven as vulnerable to Federal Reserve tapering news and the subsequent rise in U.S. Treasury yields as emerging markets debt. U.S. high-yield corporate bonds have, although they usually have shorter durations, have not been immune, either. For example, the SPDR Barclays Capital High Yield Bond (NYSEArca: JNK) is off 3% since May 22.

Rising rates have, of course, punished long duration bond funds and the resulting strength in the U.S. dollar has highlighted the vulnerability of emerging markets with widening account deficits. Since May 22, the iShares 20+ Year Treasury Bond ETF (NYSEArca: TLT) has slid 9.5% while the Market Vectors Emerging Markets Local Currency Bond ETF (NYSEArca: EMLC) has plunged 11%. [Rising Rates Weigh on Emerging Markets Bond ETFs]

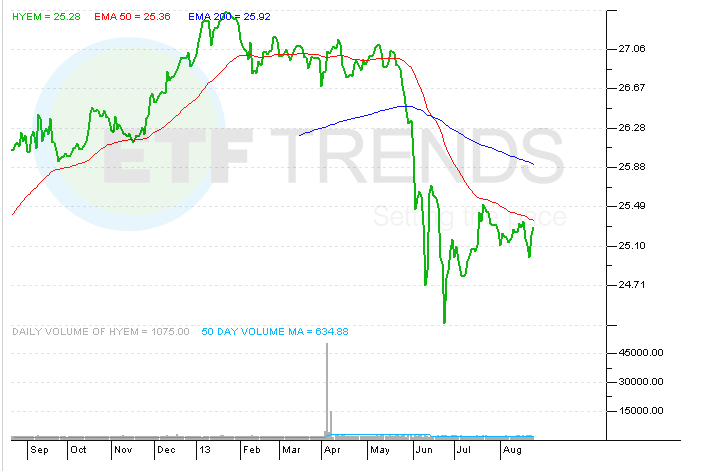

Said differently, it might be hard to imagine high-yield emerging markets not being caught in the recent bond market calamity. However, the Market Vectors Emerging Markets High Yield Bond ETF (NYSEArca: HYEM) has been less bad than the aforementioned ETFs with a 90-day loss of 6%.

HYEM debuted in May 2012 and has $214.6 million in assets under management. In fact, HYEM has raked in the bulk of its AUM total this year even as investors have pulled cash from U.S. high-yield corporate bond ETFs. HYEM has attracted over $199 million in new capital this year compared to $3.4 billion of outflows from JNK, according to Index Universe data.

Although the environment for emerging markets bonds is currently challenging, put things mildly, HYEM may offer opportunity in the future. Emerging market bonds offer higher yields than those in the U.S. and emerging market companies have lower debt levels, and the ability to pay off debt compared to U.S. corporations. HYEM’s 30-day SEC yield is 163 basis points higher than JNK’s. [Emerging Markets Bond ETFs Trump Low Treasury Yields]

HYEM’s modified adjusted duration of 4.26 years is also slightly lower than JNK’s 4.5 years. Still, investors have not been showing much faith, at least not recently, in emerging markets debt as an asset class. Since the start of June, retail investors have pulled $18.1 billion from emerging-market bond funds. [Retail Investors Dumping EM Bonds Faster Than Pros]

There are added risks with high-yield corporate debt in the emerging world. The rising dollar is expected to cause an increase in default rates on developing world corporate debt. Analysts say the most pain could be felt by utilities, retailers, consumer goods and real estate firms whose cash flows tend to be in domestic currencies, according to Reuters.

HYEM’s weight to the utilities and consumer-related sectors is about 16%. The ETF also has relatively light exposure to countries with the worst-performing currencies. Turkey, Indonesia and Brazil combine for just 7.5% of the ETF’s weight while India is not even found among HYEM’s top-20 country exposures. One reason why HYEM has been less bad than other emerging markets bond funds is that although the ETF’s holdings are primarily dollar-denominated, China, home to one of the stronger emerging markets currencies this year, is 13.7% of the fund’s weight.

Market Vectors Emerging Markets High Yield Bond ETF

{kind=link}

ETF Trends editorial team contributed to this post. Tom Lydon’s clients own shares of JNK and TLT.