Van Eck Global, as the sponsor of Market Vectors municipal bond exchange-traded funds (ETFs), naturally has serious concerns following the filing of the petition by the City of Detroit seeking protection under Chapter 9 of the bankruptcy code. What implications do I think are to be drawn?

I believe it does mean an immediate adjustment to the valuations of securities issued by the City of Detroit and its instrumentalities. The potential diminution of those values may have an impact upon some investors’ personal as well as large institutional portfolios, to varying degrees.

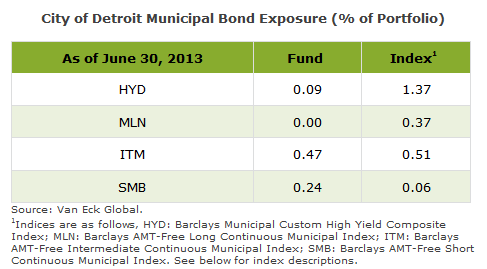

Market Vectors’ municipal bond ETFs seek to track indices constructed with a rigorous rules-based structure. The City of Detroit and some of its instrumentalities are, because of their prior creditworthiness and presence as large issuers of municipal bonds, included in these indices and, hence, are present in several of the ETFs (HYD, MLN, ITM and SMB).

The following table displays exposure of Market Vectors municipal bond ETFs to City of Detroit municipal bonds versus each ETF’s underlying index. As of yesterday (July 18), prior to the Chapter 9 filing, these issues were appropriate holdings, in my view. If the ratings agencies were to adjust the credit ratings of these issuers, many holdings may no longer be eligible for inclusion in the ETFs’ underlying indices. Such is the rules-based approach of index funds and, in particular, of ETFs. If removed from the index, and as the market allows, those securities may be removed from the ETFs.

{kind=link}

To be clear, I believe filing for bankruptcy by a municipality is not an end. Nor do I believe it necessarily means mass firings, closing of offices and shuttering of municipal services (e.g., police, fire, water, sewer and electric). It does mean, in my view, that there may now be a process, overseen and directed by a judge, to stop the clock on expenses to seek to redress the massive imbalance of revenues and obligations. I feel that Detroit may continue to function day-to-day as a going concern, relieved temporarily from some of the burden of payments. Assuming the bankruptcy court accepts and approves the Chapter 9 filing, I would expect the court to begin directing payments as needed.

The critical element underpinning this event, in my view, also fundamentally sets the foundation for the majority of all financings done in the municipal bond market. That is, of a “moral obligation” on the part of the issuer of bonds to promise to set the “full faith and credit” and taxing power of that entity ahead of other debts in order to repay the owners of those bonds. The state-appointed emergency manager of the City of Detroit has already made representations that he, and the State, may be willing to break that foundation in its effort to save Detroit and put it back on the path to financial solvency.

What is of concern to me here, and has been voiced by analysts and portfolio managers alike, is that the path chosen for Detroit may likely set a precedent for other struggling cities and communities that undermines the totality of municipal finance. Should that occur, I believe there would be damage done to untold numbers of portfolios as confidence may disappear and valuations may potentially drop.

I believe the process, to be sure, will not please everyone and pain will likely be borne. But I urge caution with regards to any precedent-breaking measures that leave a nearly $3.7 trillion municipal bond industry looking worse than Detroit in its darkest day.

James Colby is a portfolio manager and senior municipal strategist at Market Vectors ETFs.