The U.S. investment-grade corporate bond market is massive. Issuers sold $158 billion in high-grade corporate debt during the second quarter and that is 12% lower than the first-quarter tally, according to Dealogic. If that $158 billion was converted into the market capitalization of a well-known U.S. company, it would equal five General Mills (NYSE: GIS).

With a market of that size, it is not surprising that the iShares iBoxx $ Investment Grade Corporate Bond ETF (NYSEArca: LQD) has nearly 1,070 holdings. And it is not surprising that some market participants, even at the same firm, can have differing opinions of the investment-grade corporate bond market. [Investment-Grade Corporates Yield 4%]

LQD and its holdings have at least one supporter: JP Morgan. “In US high grade corporates, we are more bullish, and look for spreads to tighten further as the year progresses given increasing demand from pension and insurance buyers, less supply, limited outflows from public funds, and ongoing demand for shorter-duration instruments,” the bank said in a note posted by Michael Aneiro at Barron’s.

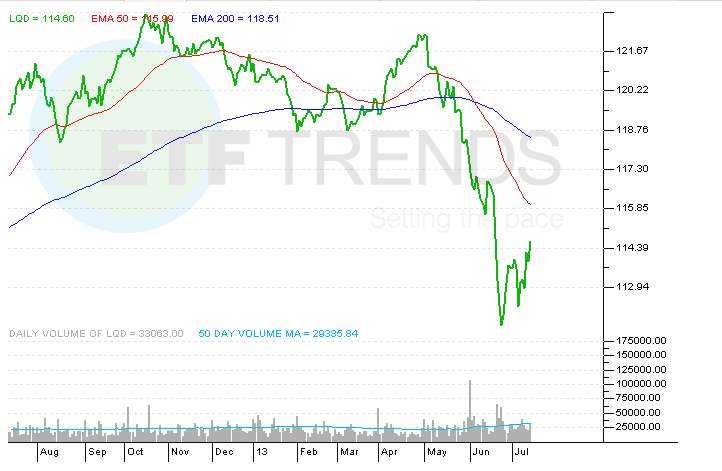

Although LQD has a weighted average duration of just 7.53 years, the ETF has proven vulnerable to rising Treasury yields. In the past three months, LQD is off nearly 5%. In March, the fund about $24 billion in assets under management. That total had fallen to $19.3 billion as of Monday. [Rising Rates Slam Corporate Bond ETFs]

Not everyone at JP Morgan, the world’s largest underwriter of corporate debt, is a fan of those bonds. Jan Loeys, who runs a global asset allocation team for the bank, says the dismal performance turned in by corporate bonds in the first half of this year could get worse, reports Lisa Abramowicz for Bloomberg.

The measuring stick for corporates is the yield advantage over Treasurys with wider spreads implying deteriorating credit quality. Conversely, narrower spreads are a sign of enhanced creditworthiness. Earlier this month, investment-grade corporate spreads were 219 basis points. LQD currently has a 30-day SEC yield of 3.52%, according to iShares data, compared to a 2.56% yield on 10-year Treasurys.

Even with an apparently narrower spread over 10-years, LQD still has to deal with the fact the Federal Reserve may curb its purchases of Treasurys and mortgage-backed securities. Combine that with elevated concerns about liquidity in the corporate bond market and investors that previously prized high-grade corporates have run for the exits.

Near-term selling pressure, should it continue, would prove Loeys correct. As it is LQD and the Vanguard Intermediate-Term Corporate Bond Index ETF (NasdaqGS: VCIT) are down an average of 2% in the past month. Long-term investors can still utilize corporate bond investments, like LQD, as part of a diversified fixed-income portfolio, but those investors must be aware of the vulnerabilities of the asset class if these bonds appear overvalued relative to Treasurys.

iShares iBoxx $ Investment Grade Corporate Bond ETF

{kind=link}

ETF Trends editorial team contributed to this article. Tom Lydon’s clients own shares of LQD.