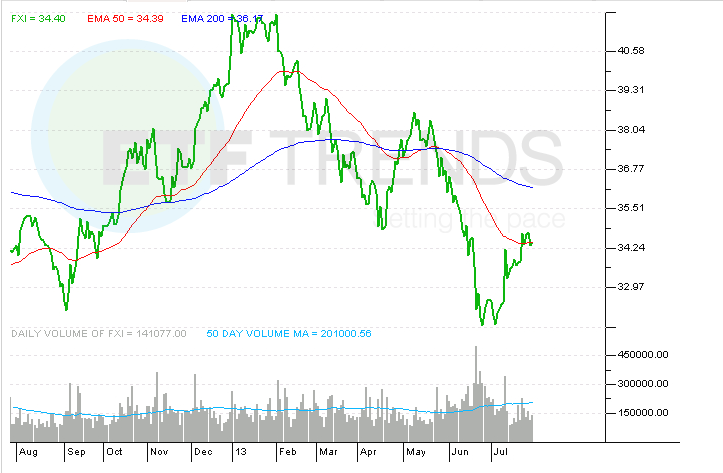

The iShares China Large-Cap ETF (NYSEArca: FXI) is up 5.8% in the past month, a impressive performance by the recent glum standards of the largest China ETF. While nice, FXI’s one-month gain is not nearly enough to erase several years of pain endured by long-term investors in China ETFs.

FXI’s recent burst of strength comes as $37 billion was pulled from emerging markets equity and bond funds last month. However, just a few days away from the anniversary of Shanghai Composite’s August 2009 peak, FXI is still sitting on a loss of almost 18% over those four years. The iShares MSCI Emerging Markets ETF (NYSEArca: EEM)is up about 10% over the same time. [Bargain Hunting in Emerging Markets ETFs]

Back in 2009, Chinese stocks, FXI and rival ETFs appeared to be ushering in a new form of dominance on the global investment landscape, but since that August 2009 peak, Chinese shares have been anything but dominant. The Shanghai Composite has tumbled 43% since then, erasing $748 billion in market value along the way, report Richard Frost and Weiyi Lim for Bloomberg.

U.S. investors can access stocks traded on China’s mainland with the Market Vectors China ETF (NYSEArca: PEK), an ETF that tracks index comprised of swaps and other derivative instruments. PEK has lost 37.4% since its October 2010 debut. [Diversified Exposure With China A Shares ETF]

To put the loss of $748 billion in lost market value into context, that is roughly equivalent to two and a half Googles (NasdaqGM: GOOG) and more than three Chevrons (NYSE: CVX).

Among China ETFs, FXI’s large allocations to state-controlled banks and energy firms have made the fund vulnerable. Following June’s spike in China’s Interbank lending rates, doubts remain about liquidity in the massive Chinese banking system. Chinese energy stocks such as PetroChina (NYSE: PTR), once the world’s largest company by market value, have been laggards compared to their U.S. rivals this year. [Analysts Miss Mark on Chinese Banks]

Financial services and energy names combine for nearly 65% of FXI’s weight. Alone, financial services commands an allocation of 52.2% in the ETF. Underscoring the vulnerability of Chinese large-caps in this glum run for the country’s stocks is this factoid courtesy of Bloomberg: No Chinese companies are found among the world’s 10 largest for the first time since 2006.

If there is a silver lining for Chinese stocks and shareholders of ETFs such as FXI it is the market’s discounts relative to the broader emerging markets universe.

“When you view Chinese stocks from the value perspective, they look cheap relative to other emerging markets and the broader market. For instance, the MSCI China index is currently trading at below 9x forward earnings, versus 10.6x for the MSCI EM index and nearly 15x for MSCI World index,” said iShares Global Chief Investment Strategist Russ Koesterich. [Why Chinese Stocks are a Value Play]

iShares China Large Cap ETF

{kind=link}

ETF Trends editorial team contributed to this post. Tom Lydon’s clients own shares of EEM and Google.