• On June 5, the Brazilian government removed the 6% Financial Transaction Tax (IOF1) on foreign exchange conversions of the Brazilian real for government bond investments.

• On June 13, the government removed the 1% tax on currency derivatives.

• We view the reduction of these barriers to entry as a positive development for the local bond market.

• More attractive accessibility could lead to lower bond yields and more efficient markets, should the clouds leading up to Standard & Poor’s negative outlook announcement2 dissipate.

After a disappointing May and June that saw many emerging market currencies depreciate against the U.S. dollar, Brazilian finance minister Guido Mantega removed the 6% Financial Transaction Tax linked to the purchase of local market fixed income securities. On June 13, the government also removed its 1% tax on currency derivatives. We view these as positive developments for Brazilian assets, given that it removes impediments to fixed income investment flows. However, the timing of such announcements has raised some red flags. Foreign participation in the local markets had stagnated at around 15%, compared to other Latin American markets such as Peru and Mexico, which have benefitted from much higher participation.3

The IOF tax was raised to 6% in September of 2010 as a primary weapon in the government’s fight against hot money flows. During his announcement about removing the tax, Mantega commented that flows had normalized and the value of the currency was not being used to combat inflation. But the change is underscored by concerns over the recent weakness in the currency (May’s 6% decline was the steepest decline since September 2011) combined with disappointing growth in the face of burgeoning inflation pressures. The central bank’s repeated intervention in currency markets and the recent move by the government on the tax side can be viewed as defensive actions sought to cap the real’s weakness. Interestingly, during the announcement, Mantega was quick to point out that the tax could be reinstated in the face of prolonged currency strength. [Brazil ETFs Lower on Protests]

Next page: Investors re-evaluate Brazil

We believe both the local bond markets and the foreign exchange rate have recently come under pressure as investors re-evaluate Brazil’s prospects over the short term. The combination of inflation remaining above the central bank’s comfort zone and economic growth projections that were recently revised down has seen dark clouds creeping over Brazilian markets. Over the past several weeks, the market has moved lower as the real weakened to levels not seen since the global financial crisis.4 However, we do not believe Brazil is facing the same types of headwinds that it was facing in 2009. Through the combination of some of the highest interest rates in Latin America and a currency that has come under pressure, we believe that Brazilian debt could provide an attractive risk/reward for medium- or long-term investors.

{kind=link}

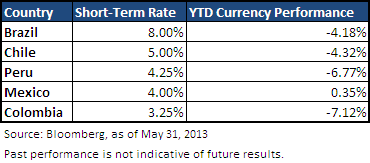

As shown in the table above, Brazil currently offers some of the highest yields in all of Latin America. While the potential for near-term volatility is still present in many of these markets, Brazil offers a potential “cushion” against further currency weakness due to its higher rates. Should some of the negative clouds regarding economic growth lift, we believe the real could trade higher than its current depressed levels.

Recently, the ratings agency Standard & Poor’s revised its ratings outlook for Brazil from stable to negative. The agency noted the potential for a continued deterioration in the growth outlook combined with Brazil’s current fiscal and external vulnerabilities as the reason for the announcement. In our view, we believe this could serve as a shot across the bow for Brazil and other EM countries to continue their efforts to further reduce external vulnerability. After a series of upgrades in credit ratings for many EM countries by the ratings agencies in the past few months S&P’s announcement has caused an already fragile market to weaken further. Even though the near-term headwinds appear to continue, we believe that Brazil may still present an attractive risk/reward near current levels.

While the impact of the announcement of the removal of the Financial Transaction Tax was muted by other market forces, we view this development as a longer-term positive for investment in the Brazilian bond market. For some investors, high levels of carry and a currency trading near multi-year highs may provide an attractive option for diversifying away from U.S. dollar-based investments.

Rick Harper is head of fixed income and currency for WisdomTree Asset Management. This post was republished with permission from the WisdomTree blog.

1IOF: Imposto sobre Operações Financeiras (Portugese)

2Standard & Poor’s, June 7, 2013.

3Source: Standard Chartered Bank, June 6, 2013.

4Source: Bloomberg, June 11, 2013.