After falling sharply over two days in mid-April, many investors are beginning to question the role that gold should play in their portfolio.

Putting this sell-off into context will comfort some, but others will ask if they can still count on gold to be the all-weather asset that they expected it to be. Gold’s recent decline was certainly steep, but it wasn’t unprecedented. In fact, gold has seen seven pullbacks of more than 10% since 2001. After each drop, gold went on to not only rebound but to post new highs. This trend highlights the need to understand both the short-term and long-term drivers of the price of gold in order to see why gold remains a key element to a diversified portfolio.

Market pundits and analysts have attributed a multitude of explanations for April’s declines. One such explanation concludes that the sell-off of Cyprus’ gold reserves would lead to other highly indebted European countries having to do the same and consequently cause gold to fall aggressively. Considering that this would require changes to current arrangements, such as the Central Bank Gold Agreement, even if this was to occur, the Cypriot contagion argument may not capture the full picture. The economic slowdown in China has also been cited as a plausible reason for the sell-off in gold. While the Chinese GDP print did come in below consensus expectations, 7.7% growth is nothing to be ashamed of in today’s environment, and would still lead to continued demand for gold from China. Another explanation puts blame on the recent outflows from exchange traded funds (ETFs) as a major influence. Considering gold ETFs and other related investments comprise only 7% of annual gold demand, this argument appears weak.

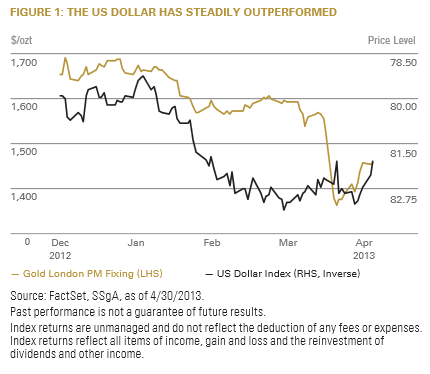

Others contend that the strength of the US dollar is the main culprit for gold’s recent weakness. Based on gold’s negative correlation to the dollar over the long-term, this may be a more plausible explanation. In 2013, gold has declined at the same time as the dollar has rallied. However, as seen in Figure 1, this correlation doesn’t do an excellent job of explaining April’s drop, because while both assets generally moved in opposite directions, the way they did so differed tremendously.

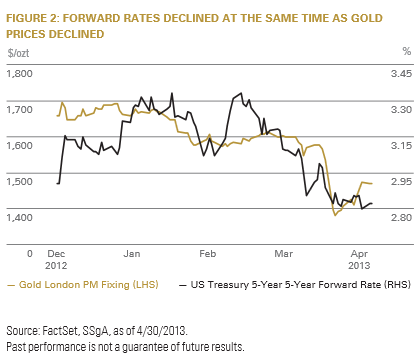

Yet, in light of the recent unprecedented, and extraordinary monetary policy measures that have been undertaken around the globe, many investors expected to see inflation run rampant. However, due to a lack of velocity, inflation has been downright subdued in many developed markets, especially in the US. In turn, near-term inflation expectations have decreased considerably. The relationship between gold and US inflation expectations this year has been strong. Considering that some investors purchase gold for its inflation-fighting characteristics, if prices are sideways or downwards, investors may begin to question an allocation to gold because they feel that gold is no longer needed as an inflation hedge, therefore providing no real utility in their portfolio.

Should the dollar continue to outperform relative to its largest trading partners, gold could face additional headwinds. At the same time inflation may be low for the time being, but the long-term impacts of quantitative easing and balance sheet expansion are unknown. While subject to controversy, there’s strong evidence to suggest that gold can protect investor’s purchasing power.

{kind=link}

However, none of these explanations solely explain gold’s recent price declines, which largely seem to be driven by a confluence of them all. These explanations also don’t foretell much about future performance. While the price of gold has stabilized and rebounded since its mid-April lows, skeptical investors should ask themselves the following questions: Do I think China and other emerging markets will no longer be the source of global growth in the future? Do I think developed market countries will stop taking extraordinary measures to combat the impacts of deleveraging? Do I think that the US dollar will exhibit a prolonged period of strength? If the answer is no, than investors who opted to or are considering selling should keep in mind that many of the fundamental reasons why gold was attractive in the past continue to remain intact today.

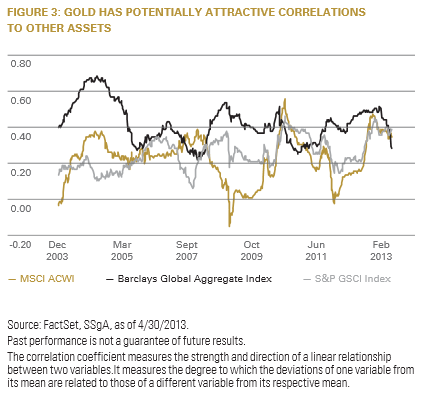

Furthermore, it’s worth considering gold’s role in portfolios, which is independent of price. Gold’s low correlation to other asset classes suggests that it has the potential to improve the efficiency of portfolios. While static correlation statistics are useful, it can be more instructive to look at rolling correlations. Under this framework, one can see how gold’s relationship to other assets may change over time. What’s interesting today is that gold’s correlation to global fixed income has been steadily dropping since the start of this year and is now below historical averages. This suggests that gold may have increased diversification benefits.

In the immediate-term, certain investors may point to gold dipping below important support levels and lacking key drivers of near-term demand. Acknowledging important evolutions that have changed the dynamics of the gold market is important to dispelling concerns brought on by these immediate- term markers. These include the creation of gold-backed ETFs that have brought liquidity, transparency and cost efficiency to the market, not just in the US, but around the world, and the liberalization of the Chinese gold market with the establishment of the Shanghai Gold Exchange. The later evolution plays an important role in outlining how geographical demand for gold in a supply-constrained market has shifted from the western world to the eastern world. At the same time, today’s demand is more balanced, with jewelry, technology, investment and perhaps most importantly, central bank purchasing, all playing a role.

In conclusion, gold may see near-term volatility as the market reassesses the level at which gold should be priced, today. Drawdowns of this nature have occurred before, and with little change to the underlying supply and demand characteristics that underpin gold’s price, gold may see better days ahead. Based on historical performance, which isn’t necessarily predictive of future results, this period may serve as a buying opportunity similar to those in past cycles. In the meantime, investors may be well served by using a pullback in an individual asset, such as gold, to review their entire portfolio and look to construct one with a combination of the best expected future risk-adjusted returns.

{kind=link}

{kind=link}