The yen’s sudden burst of strength, the CurrencyShares Japanese Yen Trust (NYSEArca: FXY) is up 6.2% in the past month, is having predictable consequences. For example, equity-based ETFs such as the wildly popular WisdomTree Japan Hedged Equity Fund (NYSEArca: DXJ) and the iShares MSCI Japan Index Fund (NYSEArca: EWJ) have been hammered. In the past month, DXJ is down 12.5% while EWJ is off 8.3%.

Another area where the yen’s rise is having glum consequences is the carry trade, the foreign currency transaction where traders short a low-yielding currency and use the proceeds to purchase a higher yielding currency. As many experienced forex traders already know, a typical carry trade would involve shorting the yen and purchasing the Australian or New Zealand dollars. ETF traders can pull that trade off with the PowerShares DB G10 Currency Harvest Fund (NYSEArca: DBV). [Yen ETFs And The Carry Trade]

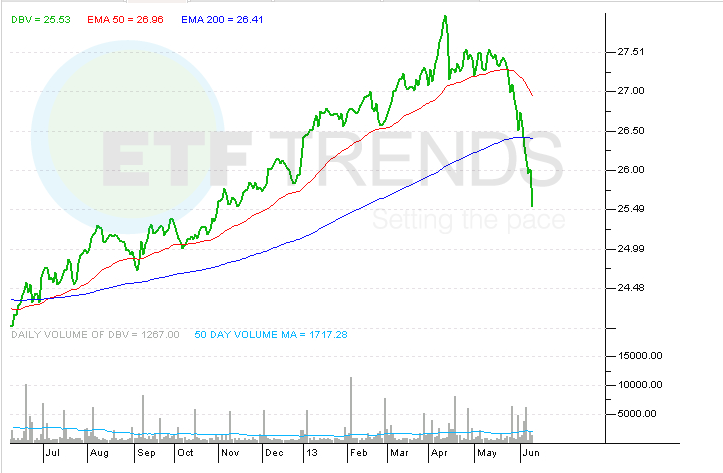

With $297 million in assets under management, DBV is one of the largest multi-currency ETFs on the market. Japan’s strident efforts to weaken the yen coupled with Australia’s struggles (New Zealand, too) with its strong dollar benefited DBV in noticeable fashion as the ETF jumped 4% in the first four months of this year. Even more impressive regarding DBV’s fast start to the year is that in addition to being the short the yen, the ETF is short the euro, a currency that has been surprisingly strong given the Eurozone’s myriad economic woes. [Concerns for Euro ETFs]

The other side of the coin is that a rebounding yen combined with extended weakness in the Aussie and kiwi have sparked a brutal carry trade unwind. “Once popular higher-yielding currencies, such as the Australian dollar, are now falling out of favor as the interest rates they offer decline and the differential with lower-yielding ‘funding’ currencies, such as the Japanese yen, narrows,” reports Nick Hastings for the Wall Street Journal.

The carry trade falling out of favor has sent DBV down 7.1% in the past month and the ETF could be vulnerable to more downside on the back of the wilting Aussie. During Wednesday’s Asian session, National Australia Bank said it expects the Aussie will fall below 93 cents against the greenback this year and 87 cents next year. NAB’s forecast comes a day after the Aussie fell to a 33-month low against the greenback, according to Investing.com.

That news came a day after Goldman Sachs said it sees the Aussie trading down to 85 cents against the greenback within a year. This is also bad news for the New Zealand dollar, 33% of DBV’s long exposure, because that currency has an intimate correlation with the Aussie.

DBV’s other long exposure, the Norwegian krone, is also worth keeping an eye on for two reasons. First, the krone is sensitive to oil price fluctuations because Norway is a major oil producer. Second, the currency has been uncomfortably strong against the euro, hurting Norwegian exports along the way, and that could force the central bank there to act.

PowerShares DB G10 Currency Harvest Fund

{kind=link}

ETF Trends editorial team contributed to this article.