Years of easy liquidity and low interest rates benefited one asset class in a big way. Master limited partnerships, or MLPs, have feasted on low rates on two fronts. First, MLPs are capital-intensive businesses and low financing costs have meant less money going out the door to service debt. That brings up the second point, which is those same low borrowing costs have meant more cash going to shareholders in the form of dividends.

It has been those steadily rising payouts and juicy yields that have sent so many investors into MLPs and related ETFs and ETNs in what has previously been a low interest rate environment. Assets under management tallies tell the tale. For example, the JPMorgan Alerian MLP Index ETN (NYSEArca: AMJ), with a yield of almost 4.7%, has nearly $3.1 billion in assets. The Alps Alerian MLP ETF (NYSEArca: AMLP) yields 5.87% and has over $6.3 billion in assets. [A Closer Look at MLP ETFs]

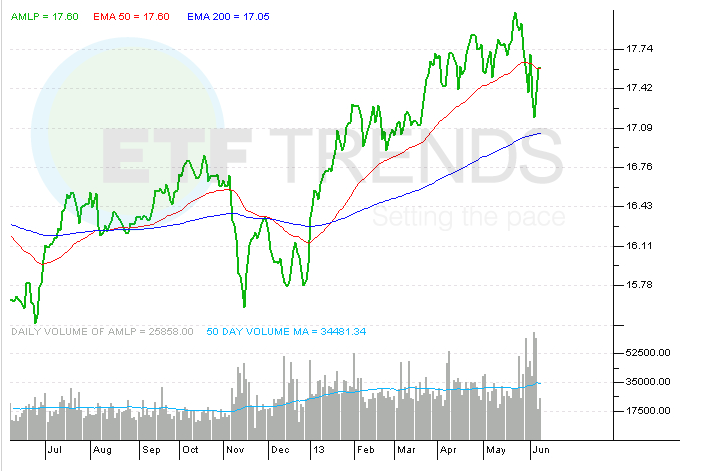

Rising rate fears have taken some of the wind out of the MLP trade. From May 20 through June 5, AMJ tumbled 7.7% while AMLP lost about 4%. Both have subsequently rebounded a bit, but it could take more than just a few days of positive price action to calm investors’ nerves about rising interest rates and the ensuing impact on MLPs. [MLP ETFs: Attractive Yields And Risks]

Next page: Risk factors

The universal assumption is that MLPs of all shapes and sizes are vulnerable to rising interest rates, although multiple factors must be taken into consideration. Those MLPs with high debt-to-equity ratios and large amounts of floating rate debt would be most vulnerable. Additionally, investors that want to remain in the MLP game if rates do rise should consider those names with exposure to multiple oil and natural gas producers.

That group would include some of the largest MLPs such as Enterprise Products (NYSE: EPD), Kinder Morgan (NYSE: KMP) and Plains All American (NYSE: PAA). Those three stocks combine for over 25% of the Alerian MLP ETF’s weight, according to issuer data.

Indeed, smaller, highly leveraged MLPs with exposure to floating rate debt that are dependent on just one or two energy companies for the bulk of their revenue could be punished if rates spike. There is also some precedent for MLPs performing well as rates rise.

“Master limited partnerships (MLPs) outperformed the S&P 500 during mid-2004 and mid-2007, the most recent period of rising interest rates in the past 20 years,” Lee Jackson reported for 24/7 Wall Street, citing Credit Suisse.

Alerian MLP ETF

{kind=link}

ETF Trends editorial team contributed to this report. Tom Lydon’s clients own shares of AMLP.