Recently, we shared our prediction that the US ETF industry could experience more than 100% growth in the next five years, from current assets of $1.5 trillion to $3.5 trillion by the year 2017.

There are several key drivers fueling this growth, including increased institutional usage, the growth of the self-directed investor market and the notable opportunity that exists in the fixed income (FI) category.

This last topic is something we’ve discussed at length on the iShares Blog. As more and more investors become comfortable with bond ETFs and, more importantly, aware of the benefits they can provide, we’re seeing a large increase in adoption on the FI side. In fact, bond ETFs now account for 17% of global ETP assets up from just 5% in 2005.

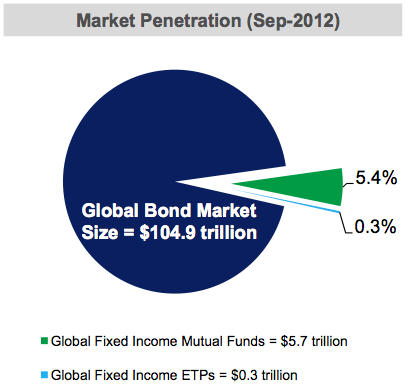

But even with this increased adoption, global assets in the FI ETF space only account for 0.3% of the underlying global bond market. You read that right – it’s really only 0.3%, and traditional mutual funds (which had a considerable head start) only weigh in at 5.4% (see below).

{kind=link}

So what exactly does this mean for current and future bond ETF investors? The first implication is that there is obviously a lot of runway for future growth, and as bond ETFs grow in assets there can be potential benefits for investors (increased secondary market liquidity, for example). In addition, we should continue to see the trend of ETF providers exploring uncharted territories in the bond market, allowing investors to gain new, different and precise exposures through an ETF vehicle.

The second implication is that no matter how big some fixed income ETFs have become (and some have become very big), they still only represent a very small portion of the FI universe, and therefore would not be capable of “moving” the underlying market in a meaningful way. This concern typically comes up when there are large creations or redemptions in a particular fund or ETF category – investors sometimes fear that this will cause excess buying or selling pressure on the bonds in that category, creating a “tail wagging the dog” type of scenario.

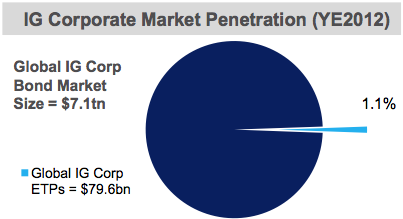

For example, the iShares Investment Grade Corporate Bond ETF (LQD) – which is the largest FI ETF – has fallen prey to this myth on occasion. But as you can see below, the entire investment grade ETF category only made up 1.1 % of the entire IG corporate bond market as of 12/31/12, with LQD only accounting for 0.3%. In addition, the majority of trading activity in LQD actually occurs on the secondary market where existing fund shares are transferred between buyers and sellers, which has no direct impact on the underlying securities. Year to date, on average 86% of LQD’s trading activity occurred on the stock exchange.

{kind=link}

Of course, these days we hear this myth much less frequently than we used to. Investors have started to realize that the dual layer of liquidity offered by ETFs is actually a benefit to them. The fact that ETFs offer liquid access and the ability to price in new information on a real-time basis, even when the underlying bonds are trading thinly or not at all, is one of the reasons we’re seeing such increased adoption of fixed income ETFs.

Dodd Kittsley, CFA, is the Head of Global ETP Market Trends Research for BlackRock.