Rising Treasury yields and talk of the Federal Reserve tapering its bond purchases have hit fixed-income ETFs across the board. However, high-yield funds are falling harder than Treasury ETFs of similar durations as credit spreads widen a bit.

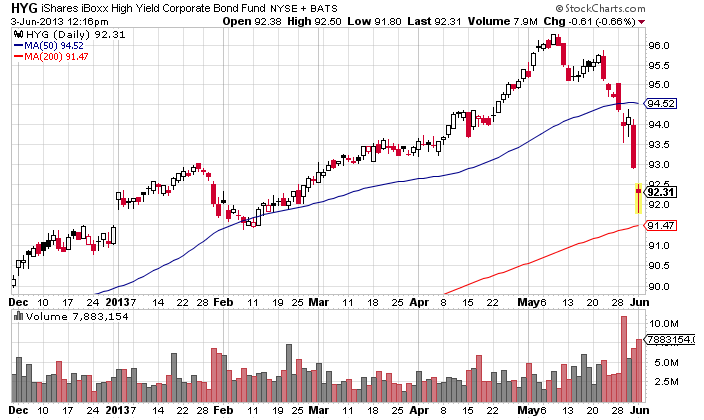

The iShares iBoxx High Yield Corporate Bond (NYSEArca: HYG) is down 3.3% for the trailing month, more than doubling the loss suffered by iShares Barclays 3-7 Year Treasury Bond (NYSEArca: IEI) during the same period. HYG, the high-yield fund, has an effective duration of about 4 years.

SPDR Barclays High Yield Bond (NYSEArca: JNK) is another large ETF indexed to junk bonds. Trading volume in JNK and HYG has picked up recently.

The high-yield ETFs have consistently outperformed Treasury bond ETFs with similar durations since late 2011. This has caused the yield spread between corporate junk bonds and Treasuries to narrow as investors take on more risk in search of yield in a low-rate environment.

However, the junk bond ETFs have underperformed the past couple weeks as credit spreads widen somewhat. Bond prices and yields move in opposite directions.

Junk bond funds such as JNK “are taking a beating,” writes Jordan Wathen at the Motley Fool. “It’s important that investors understand why certain asset classes are moving lower. While the Fed is partially to blame – higher rates mean falling bond values – the Fed’s exit has more to do with liquidity than it does higher interest rates.”

If the Federal Reserve pulls back on quantitative easing, “junk bond defaults could rocket higher,” Wathen added.

HYG is currently paying a 30-day SEC yield of 4.44%, compared with 0.63% for IEI, the 3-7 Year Treasury ETF.

Soaring demand for speculative-grade credit has pushed nominal yields down to extremely low levels.

Next page: Junk bond record issuance

“Global junk bond issuance is at record highs this year—and thus at the greatest danger should yields start rising,” reports Jeff Cox at CNBC.com.

Investors have already reacted to hints the Fed may scale back its QE program by punishing the riskiest bonds, including high-yield ETFs.

Still, some analysts say it would be premature to give up on high-yield credit, as long as investors are cognizant of the potential risks.

These risks include credit spreads widening and higher corporate default rates. [High-Yield Bond ETFs: S&P Still Sees Opportunities]

“High yield spreads are historically tight, at levels not seen since the fall of 2007 … meaning there’s currently a much smaller difference in yield between a high yield bond and a comparable Treasury,” Russ Koesterich, BlackRock chief investment strategist, said in May. “At the same time, some high yield prices have reached all-time highs. In other words, investors aren’t being rewarded that much for holding high yield, traditionally viewed as a risky asset class.”

However, he doesn’t think investors should abandon their allocation to high-yield bonds. The strategist said high-yield companies aren’t so junky anymore, all bonds look expensive, there are few alternatives for yield, and that the asset class isn’t as volatile as it used to be. [iShares: Four Reasons to Still Hold High-Yield ETFs]

iShares iBoxx High Yield Corporate Bond

{kind=link}

Full disclosure: Tom Lydon’s clients own HYG and JNK.