Exchange traded funds comprised of emerging markets sovereign debt such as the dollar-denominated iShares J.P. Morgan USD Emerging Markets Bond Fund (NYSEArca: EMB) and the local currency Market Vectors EM Local Currency Bond ETF (NYSEArca: EMLC) have been punished on news that the Federal Reserve’s easy money well could run dry in the next few months.

Emerging markets corporate bonds and the corresponding ETFs have barely been better. The WisdomTree Emerging Markets Corporate Bond Fund (NasdaqGS: EMCB) is the largest of three ETFs offering exposure to developing world corporates and that fund is down 6.8% in the past month. Obviously that is nothing to break about, but it is better than EMB’s 12.1% tumble. [Emerging Markets Bond ETFs to Consider]

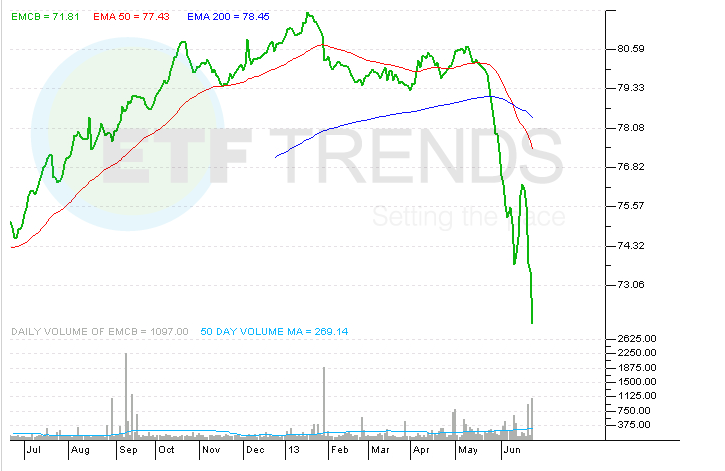

EMCB debuted in March 2012 and now has $125.6 million in assets under management. In terms of duration, or its sensitivity to rising interest rates, EMCB has an effective duration of 5.77 years compared to 7.52 years for the iShares iBoxx $ Investment Grade Corporate Bond Fund (NYSEArca: LQD). The lower duration might explain why EMCB has been able to keep pace with LQD over the past month despite the former’s obvious exposure to downtrodden emerging markets.

There are still risks with emerging markets corporate bonds, particularly in an environment of dollar strength. Emerging markets corporates have, at times, had lower default rates than sovereign debt. However, yields on those bonds have blown out compared to U.S. Treasurys on rising default fears. EMCB has 30-day SEC yield of 4.72% compared to a yield of 2.55% on 10-year Treasurys.

Although many developing world issuers of corporate debt in local currencies hedge their dollar exposure, constant hedging is expensive and much of the recent corporate borrowing in emerging markets has been by junk-rated borrowers. Possible trouble spots include China, Indonesia and Turkey, reports Sujata Rao for Reuters.

Nearly two-thirds of EMCB’s holdings are rated investment-grade. At the country level, Russia and Brazil combine for over 53% of the ETF’s weight. Both country’s have investment-grade ratings, which is important because as Moody’s Investors Service notes, there are correlations between sovereign credit stress and corporate ratings in the emerging world, according to Rob Minto for the Financial Times.

Even if corporates defaults rise in earnest, EMCB may be able to remain sturdy because the bulk of its holdings are quasi-sovereigns, or bonds issued by state-run enterprises. It is just one example and it is far from the best oil stock, but the chances of the Brazilian government allowing Petrobras (NYSE: PBR) to default on its debt are minimal because that would likely impact Brazil’s sovereign rating. Petrobras is an EMCB holding.

That does not mean EMCB is free of risk, but when the emerging markets calamity passes, the ETF’s recent sturdiness shows it might be one of the bond funds to scoop up when more docile times arrive for developing nations.

WisdomTree Emerging Markets Corporate Bond Fund

{kind=link}

ETF Trends editorial team contributed to this post. Tom Lydon’s clients own shares of EMB and LQD.