Speculation that the Federal Reserve is mulling winding down or an outright end to its asset-buying activities has weighed on mortgage REIT ETFs recently. Funds previously prized for high yields tumbled last week because mortgage-backed securities are vulnerable to rising interest rates.

The iShares FTSE NAREIT Mortgage Plus Capped Index Fund (NYSEArca: REM) and the rival Market Vectors Mortgage REIT Income ETF (NYSEArca: MORT) fell more than 4% last week.

Woes for REM, the larger of the two ETFs almost $1.2 billion in assets, and MORT can in part be attributed to quantitative easing tapering concerns plaguing individual mortgage REIT stocks. Annaly Capital (NYSE: NLY) and American Capital Agency (NasdaqGS: AGNC) sold off last week with American Capital down 6.5% for the week at one point. [Mortgage REIT ETFs: Yields And Risks]

Those two stocks account for massive percentages REM and MORT’s respective weights. REM devotes 37.4% of its weight to those stocks while the pair accounts for over 30% of MORT’s weight. [Comparing Two High Yield Mortgage REIT ETFs]

REM and MORT are not the only ETFs to have suffered due to the tapering talk. The iShares Barclays MBS Bond Fund (NYSEArca: MBB), while not down by much for the week, has endured some volatility. MBB, home to $6.52 billion in assets, offers exposure to U.S. agency mortgage-backed bonds, including Government National Mortgage Association (GNMA), Federal National Mortgage Association (FNMA) and Freddie Mac (FHLMC) securities.

That may not be a good thing as low interest rate MBS are among the assets the Fed has been buying.

Mortgage-backed securities also are the most vulnerable to rising benchmark rates because the underlying loans aren’t likely to be refinanced as often, leaving investors saddled with low-returning assets longer than expected , Al Yoon reported for the Wall Street Journal.

What could weigh on ETFs such as MBB going forward is that rising interest rates translate to higher rates on consumer mortgages. The yields on MBS that investors see are the rates at which banks sell those bonds to Fannie and Freddie. The higher the rates, the more Fannie and Freddie pay and that trickles down to the borrower.

The Fed has been buying $40 billion in MBS per month, which has been a boon for MORT and REM as the two ETFs are up an average of 19.5% in the past year. For now, the issue may not be a Fed exit from the MBS market, but rather if the exit comes sooner than investors would like, American Capital’s Gary Kain said in an interview with Bloomberg.

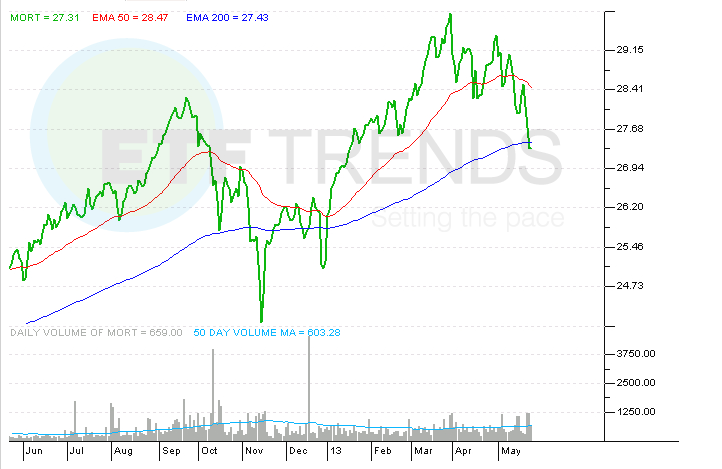

Market Vectors Mortgage REIT Income ETF

{kind=link}

ETF Trends editorial team contributed to this article.