{kind=link}

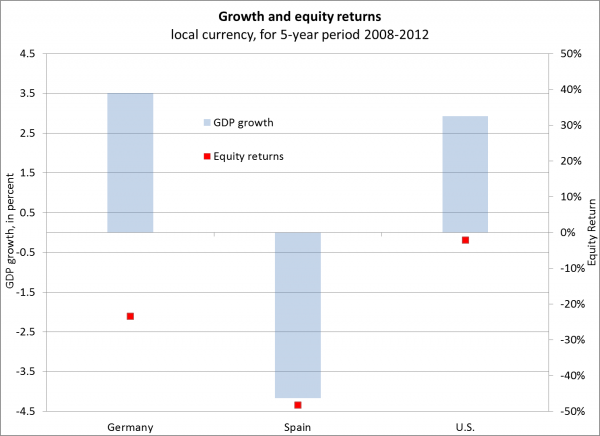

Many investors find it surprising that Spain’s public debt levels are lower than those of Germany and the United States. The association between poor economic performance and public debt levels has become a strong part of how investors think about markets — a testament to the popularity of the work that RR and others have published in the last few years.

2. Correlation is not the same as causation

For all the hoopla surrounding the Excel error, the most interesting part of the debate is not whether high public debt is associated with low economic growth (the preponderance of the evidence suggests that it is), but which causes which. Indeed, recent work by a number of academics suggests that the observed relationship may well be partly explained by low-growth countries accumulating public debt as opposed high public debt causing low growth.

In particular, if some of the relationship documented by RR arises from low-growth causing public debt, then the timing of debt-reduction programs may have significant impact on a country’s economic performance. This is because the benefits from public debt reduction may well be made up by the short-term impact of reduced government expenditure. Investors looking at the nature of debt-reduction programs when assessing their allocation to international markets should take care to note both the timing as well as the size of debt-reduction policy. We have cautioned in our own work that while long-term debt reduction should be on the menu for most developed countries, too much austerity too quickly can be counterproductive.

3. Don’t judge the book by its cover

Whatever the final outcome might be of this controversy, investors would be remiss in writing off RR’s larger body of work. Their 2009 book on the history of economic crises made a significant contribution to economists’ understanding of the nature of economic cycles — especially the differences in the shape and speed of economic recovery after downturns that are linked to a banking crisis. RR provided unprecedented depth and empirical support for the idea that banking crises are followed by very slow recoveries, a prediction that has proven all too accurate since the financial crisis.

A key finding of that body of work is that the nature of a banking crisis induces slow recovery for a wide range of reasons, including the need to repair balance sheets across private markets and individuals as well as regulatory, institutional and political changes that tend to follow banking crises.

The upshot is that investors should still be prepared for what is likely to be a continuation of the slow growth environment that we have seen over the the last five years. High public debt levels may or may not make the problem worse at the 90% GDP threshold. But either way a range of other post-banking-crisis issues remain, including only a very gradual working out of private debt overhangs, regulatory changes and higher-than-normal unemployment.

Daniel Morillo, PhD, is the iShares Head of Investment Research.