When most people think of exchange traded products (ETPs), the first thing that comes to mind is often an ETP based on a market capitalization weighted index – the S&P 500, for example.

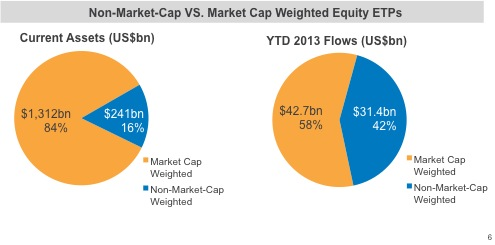

And with good reason – most of the first ETPs tracked these more traditionally weighted indexes, and today market cap weighted ETPs account for about 84% of equity ETP assets globally.

But while market cap has historically been the most popular weighting scheme for indexes, over the years the ETP industry has brought more and more products to market that are based on non-market cap weighted indexes.

Examples of this include indexes that are price weighted, fundamentally weighted (e.g. dividend weighted) and low volatility strategies.

And it appears that investors are taking notice of this diverse and dynamic category: Year-to-date, non-market cap weighted equity ETPs have captured 42% of equity ETP flows, compared with the 20% of flows they brought in last year (see below).

{kind=link}

{kind=link}

One of the more interesting trends in this category has been the increased interest in ETPs that offer exposure to a minimum volatility strategy. These products seek to track indexes that weight securities based on their tendency toward volatility, with the goal of minimizing volatility in the portfolio.

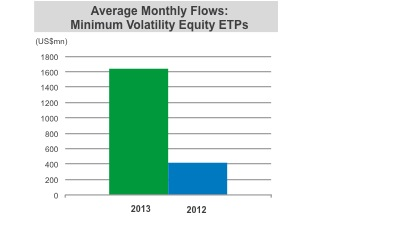

We’ve been following this trend closely since the first minimum volatility ETF was launched in May 2011, and continue to see assets flow into these products as more investors learn about their potential benefits. Minimum volatility ETPs have experienced steady inflows so far in 2013, attracting average monthly flows of $1.6bn – more than triple the average monthly flows of $416mn they received in 2012 (see below).

{kind=link}

So where is this increased interest in minimum volatility ETPs coming from? Market conditions – specifically, increased volatility – have certainly played a role in the growing popularity of these products. However, it’s a common misconception that minimum volatility ETPs are just for volatile markets, when really they have features that can potentially benefit a portfolio on a long-term basis. For example, historically some of these indexes have experienced better risk-adjusted returns than their market cap-weighted counterparts.

Of course, we believe ETPs that track the more conventional, market cap weighted indexes will continue to play an important role in portfolios. In fact, with ETP inflows on track for another record-breaking year, we think this non-market cap ETP trend is indicative of investors using more ETPs overall as part of their investment strategies. And with more and more intriguing, potentially beneficial options to choose from, we should continue to see that trend increase, as well.

Dodd Kittsley, CFA, is the Head of Global ETP Market Trends Research for BlackRock.