As a number of market watchers have pointed out recently, high yield doesn’t look so junky anymore.

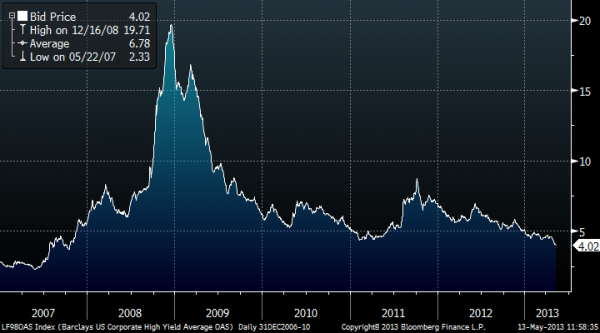

High yield spreads are historically tight, at levels not seen since the fall of 2007 as the chart below shows, meaning there’s currently a much smaller difference in yield between a high yield bond and a comparable Treasury.

At the same time, some high yield prices have reached all-time highs.

In other words, investors aren’t being rewarded that much for holding high yield, traditionally viewed as a risky asset class.

Does this mean it’s time for investors to abandon high yield? I continue to believe investors should have an allocation to high yield for four reasons:

1.) High yield companies aren’t so junky anymore. Today’s tight high yield spreads are justified given high yield companies’ historically low default rates, which are thanks to an improving US economy, ample liquidity and very strong corporate balance sheets.

2.) All bonds look expensive today. Absolute yields are close to record lows across the fixed income space as a result of continued bond buying by central banks around the world, from the Federal Reserve to the Bank of Japan. But while high yield appears fully priced, it still provides reasonable compensation — versus other fixed income alternatives — over the long term.

3.) High yield has few alternatives. For yield hungry investors, there are few alternatives to high yield considering today’s record low Treasury and sovereign yields.

4.) High yield isn’t as volatile as it used to be. While the bonds’ yields have fallen in recent years, their volatility has also dropped. In fact, the volatility of a high yield bond is roughly half of what it was last summer.

To be sure, the asset class is not without its risks. These include higher default rates than traditionally safer fixed income classes, a potential reduction in liquidity when the Fed begins to wind down its asset purchase program, and potential sensitivity to rising interest rates. Also, if the economy turns south, high yield will likely be hurt more than other fixed income sectors.

As such, high yield is not for everyone. For speculative grade exposure that may help to insulate a portfolio in the event that rates continue to rise, I prefer floating-rate notes and bank loans over high yield. In addition, while high yield should be a key holding for more aggressive investors, I advocate that risk-adverse investors hold relatively small allocations. One way to access high yield is the iShares High Yield Corporate Bond Fund (NYSEArca: HYG).

{kind=link}

The chart above shows the Barclays US Corporate High Yield Average OAS through 3/13/2013. OAS stands for Option-Adjusted Spread, or the amount by which a bond’s yield exceeds the yield of a similar duration Treasury when accounting for any optionality embedded in the bond.

Russ Koesterich, CFA, is the iShares Global Chief Investment Strategist.

The author is long HYG.