Previously I have talked about the recent concerns over rising interest rates. Although I don’t think that a significant rise is imminent, I do think that it is helpful for investors to think about strategies to help protect their portfolios during a rising rate environment.

With interest rates at near all-time low levels, many investors are afraid of price losses on bonds if rates increase. Questions remain as to how long the Fed will continue with its asset purchase program, which has contributed to lower long-term rates. As I noted in a recent post, rates have risen during the first quarter over the past three years and then ended up lower by year-end. But this pattern will not continue forever, and at some point we will be faced with a rising interest rate environment. So what is an investor to do?

Broadly there are two strategies an investor can implement using ETFs to help protect a fixed income portfolio when rates rise: sector allocation and reducing interest rate risk. In this post I’ll be covering the former, and we’ll tackle the latter in a future post.

Sector allocation is the process of shifting assets to sectors that have historically reacted more favorably in specific environments. For example, during a recession investors might want to buy high quality or risk-free assets, such as US Treasuries. Since these assets are perceived as less risky, investor demand for them tends to rise during risk-off periods, causing their prices to increase. This well-known effect is called flight-to-quality.

So how can an investor use sector rotation during a rising rate period? By rotating some assets out of fixed income sectors that tend to underperform in this kind of environment and into sectors that tend to benefit. Typically during rising rate environments, the Fed is raising the federal funds rate in response to high growth or inflationary pressures. Positive economic growth means credit conditions improve leading to a tightening (improvement) in credit spreads. Credit spreads are the incremental yield an investor demands to hold a risky asset over a similar duration risk-free bond. So while Treasury rates are increasing, tightening credit spreads can lead to stronger performance from credit investments such as corporate and high yield bonds.

Next page: When rates rise

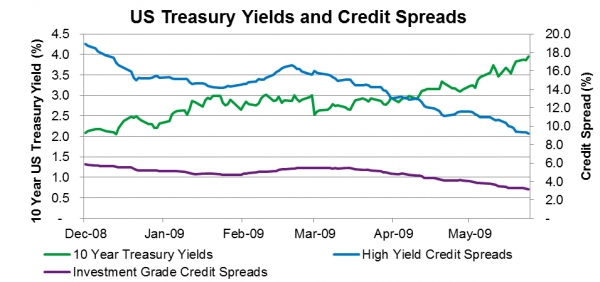

For example, during the last period of rising rates from December 2008 through June 2009, yields on 10-year US Treasuries increased from 2.08% to 3.95%. Rates were increasing as investors were moving from safer assets into riskier ones as the economy recovered from the financial market dislocations of Q4. Credit spreads also tightened with investment grade spreads declining from 5.89% to 3.15%, and high yield spreads declining from 18.95% to 9.19%.

{kind=link}

Source: Blackrock, Bloomberg and Barclays as of 4-11-2013. 7-10 Year Treasuries return represented by the Barclays 7-10 Year Treasury Index. Investment grade credit represented by the Barclays US Corporate Bond Index. High Yield represented by the Barclays US High Yield Corporate Bond Index.

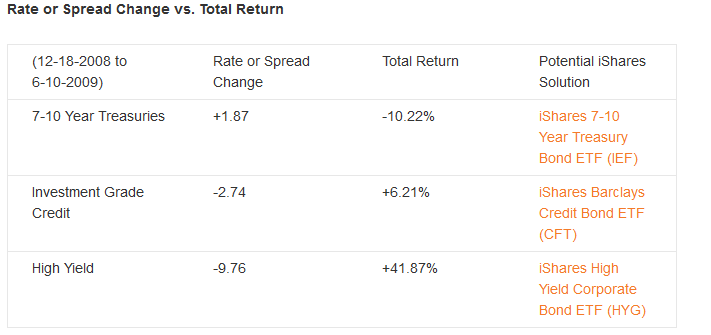

As a result of these increases in US Treasury yields, returns on 7-10 year US Treasuries fell by 10.2%. With credit spreads declining on investment grade credit and high yield, both sectors had positive total returns of 6.21% and 41.8%, respectively. While this situation was extreme in terms of the magnitude of credit spread tightening, especially in high yield, it illustrates the often-observed rise in the risk-free rate accompanied by tightening credit spreads.

{kind=link}

Another sector to rotate into might be even higher risk asset classes that would also benefit from spread tightening, such as emerging market debt (such as the iShares Emerging Markets Bond ETF, or EMB). Layering in ETFs in these asset classes can help offset price losses from rising risk-free interest rates as more of their yield comes from the credit spread. However, be aware that you are trading off interest rate risk for credit risk within a portfolio by employing these strategies. A deterioration in the economy and the credit market could adversely impact such a portfolio.

Hopefully this has post has provided more clarity on how to think about asset allocation in a rising interest rate environment. In my next post, I will illustrate how to use ETFs to reduce interest rate risk when rates increase.

Matt Tucker, CFA, is the iShares Head of Fixed Income Strategy.