In my last post, I highlighted sector rotation as a potential ETF strategy for a rising interest rate environment. This time, I’d like to focus on another common strategy for helping to protect a portfolio against rising rates: Reducing the duration, or interest rate risk, of a portfolio.

This has been a popular strategy so far this year – flows into fixed income ETFs year-to-date have been primarily into shorter duration ETFs as investors look to cut interest rate risk in their portfolios. Through April 10th, $10.2 billion has been allocated to short duration ETFs while $2.8 billion has been redeemed from longer duration ETFs. Clearly investors are voting with their dollars.

This strategy can be accomplished by selling longer duration investments in favor of shorter duration ones, or by just adding shorter duration investments to bring down average portfolio duration. As longer duration investments generally offer more yield, such a move will generally result in a lower yielding portfolio. Investors who position in this way believe that the yield they give up will be more than made up for by avoiding the price loss that a longer duration portfolio would experience in a rising interest rate environment.

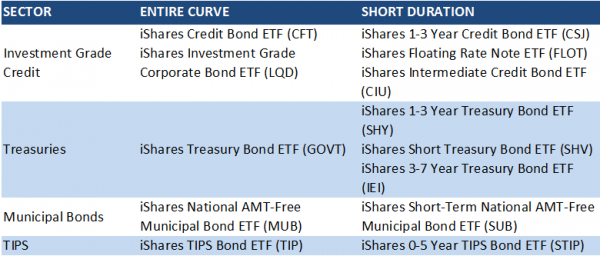

Yield curve positioning is a strategy that many institutional investors employ to position for rising rates. But using fixed income ETFs, pretty much any investor can make similar changes to their portfolios. Within different ETFs, investors can now get access to the entire yield curve or just the short maturity portion. For example, the iShares Treasury Bond ETF (GOVT) holds US Treasury bonds from 1-30 years, while the iShares 1-3 Year Treasury Bond ETF (SHY) is just the short end of the curve. The table below has ETF options for buying the whole curve or short duration funds within investment grade credit, Treasuries, municipal bonds and Treasury Inflation Protected Securities (TIPS).

{kind=link}